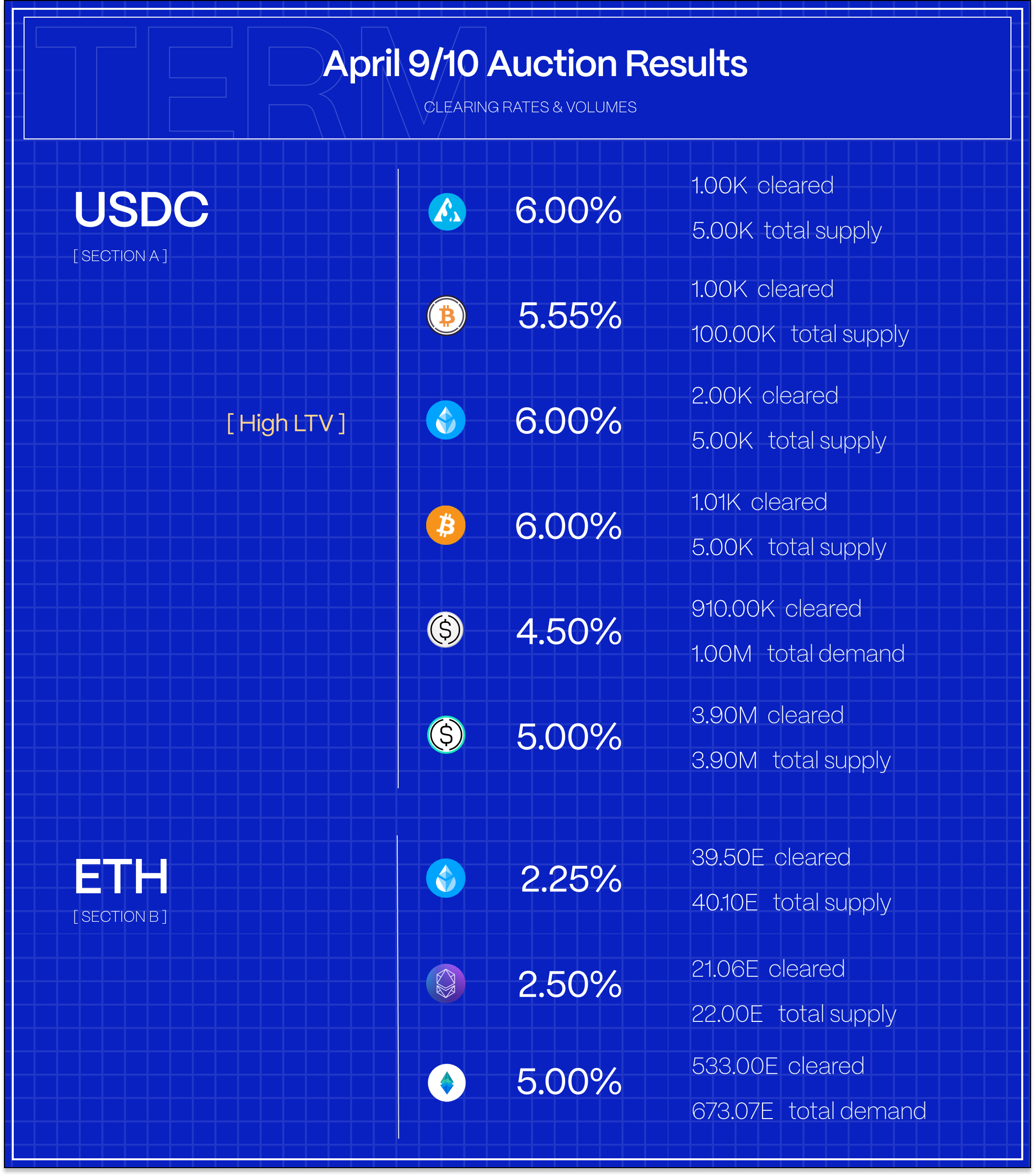

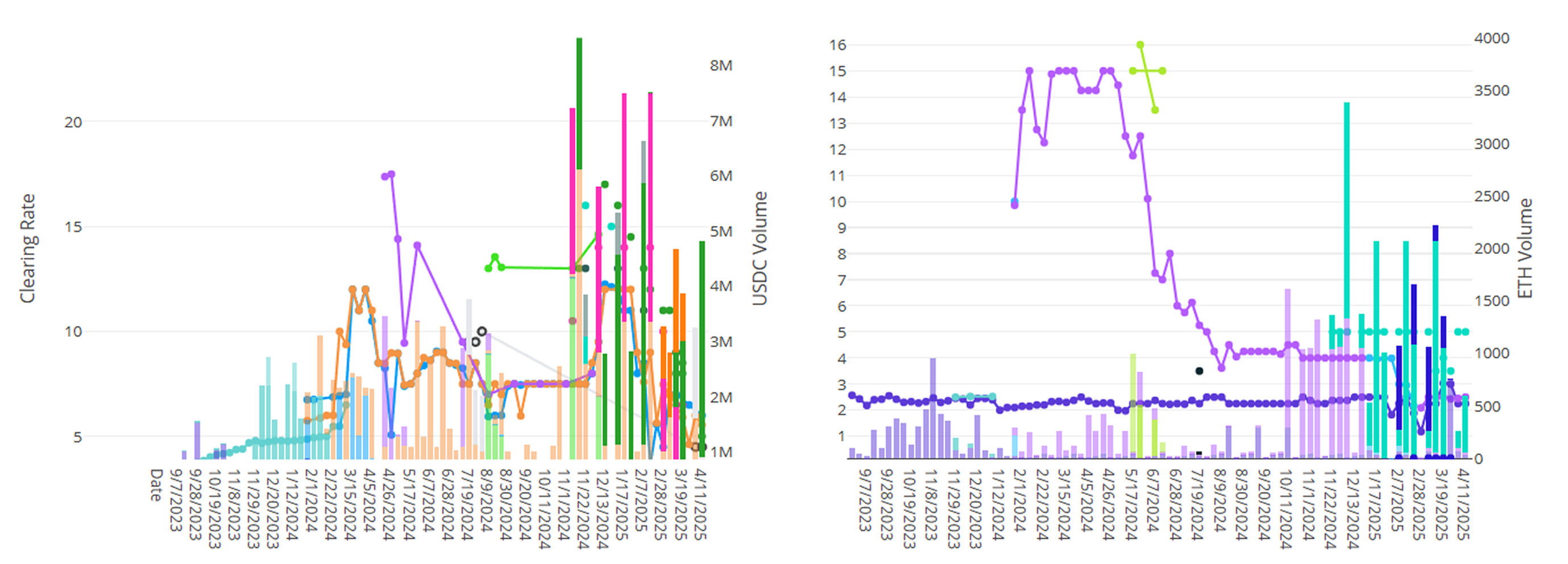

USDC volumes picked up this week on Term, with ~4M USDC clearing against both sUSDE and USDE-PT tokens. In ETH markets, demand to borrow against tETH remains robust and clearing rates remain at a healthy spread over ETH staking rates. On the vaults side, this week also saw the launch of ETH vaults on Term, which kicks off its inaugural week with 500E in supply.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

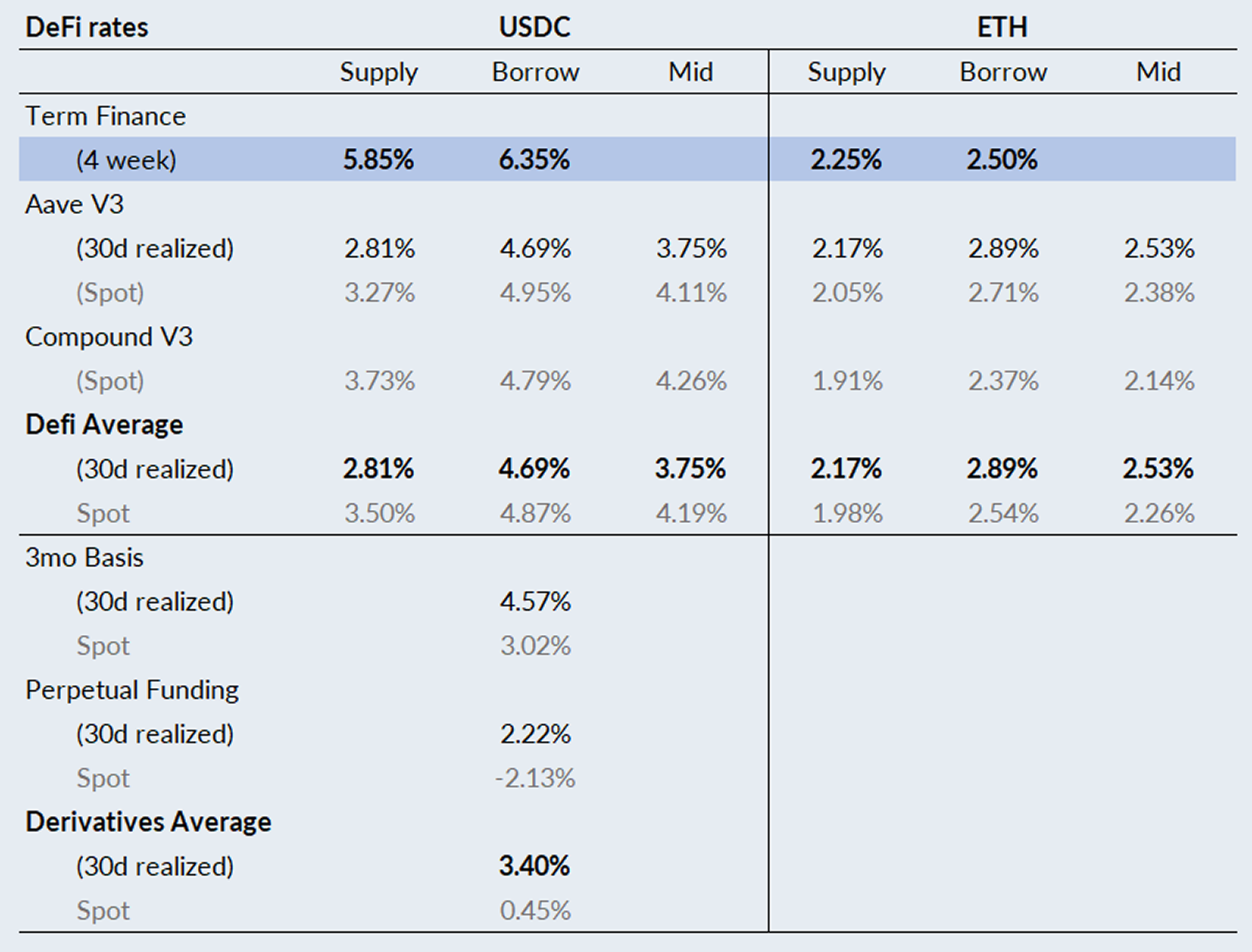

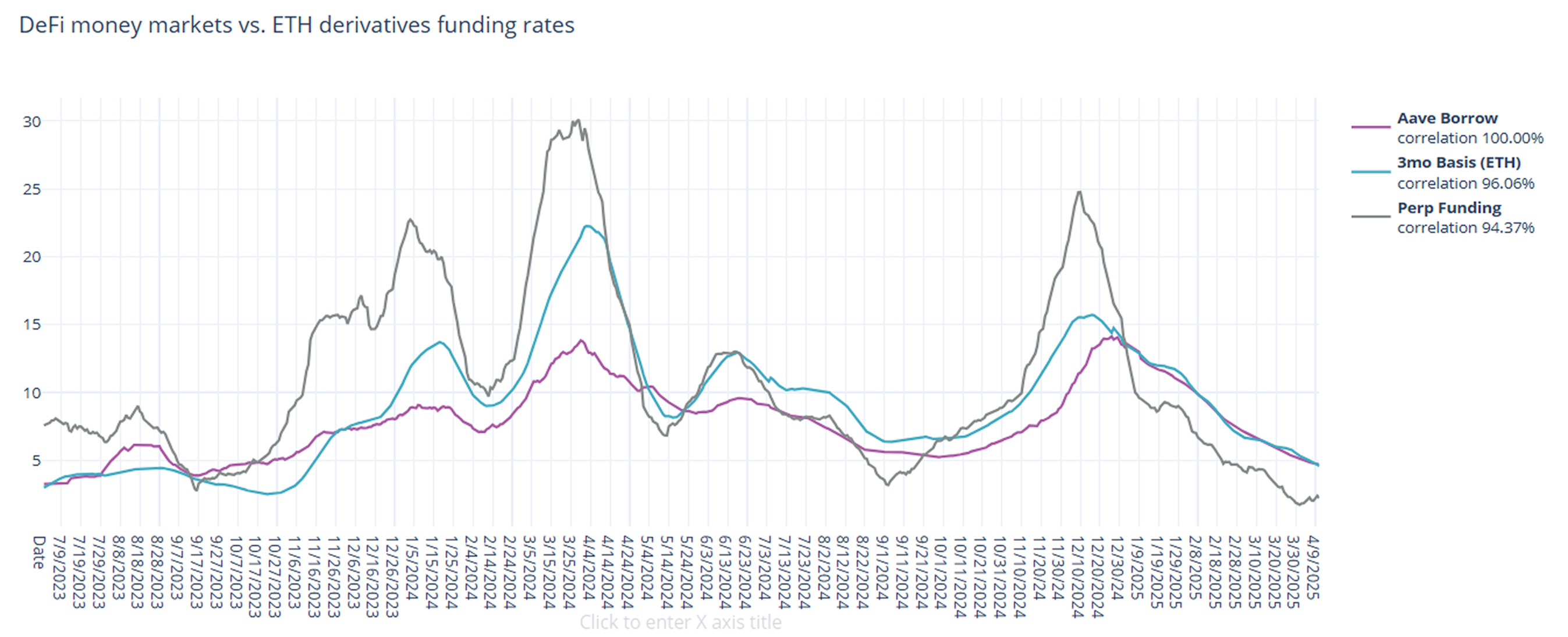

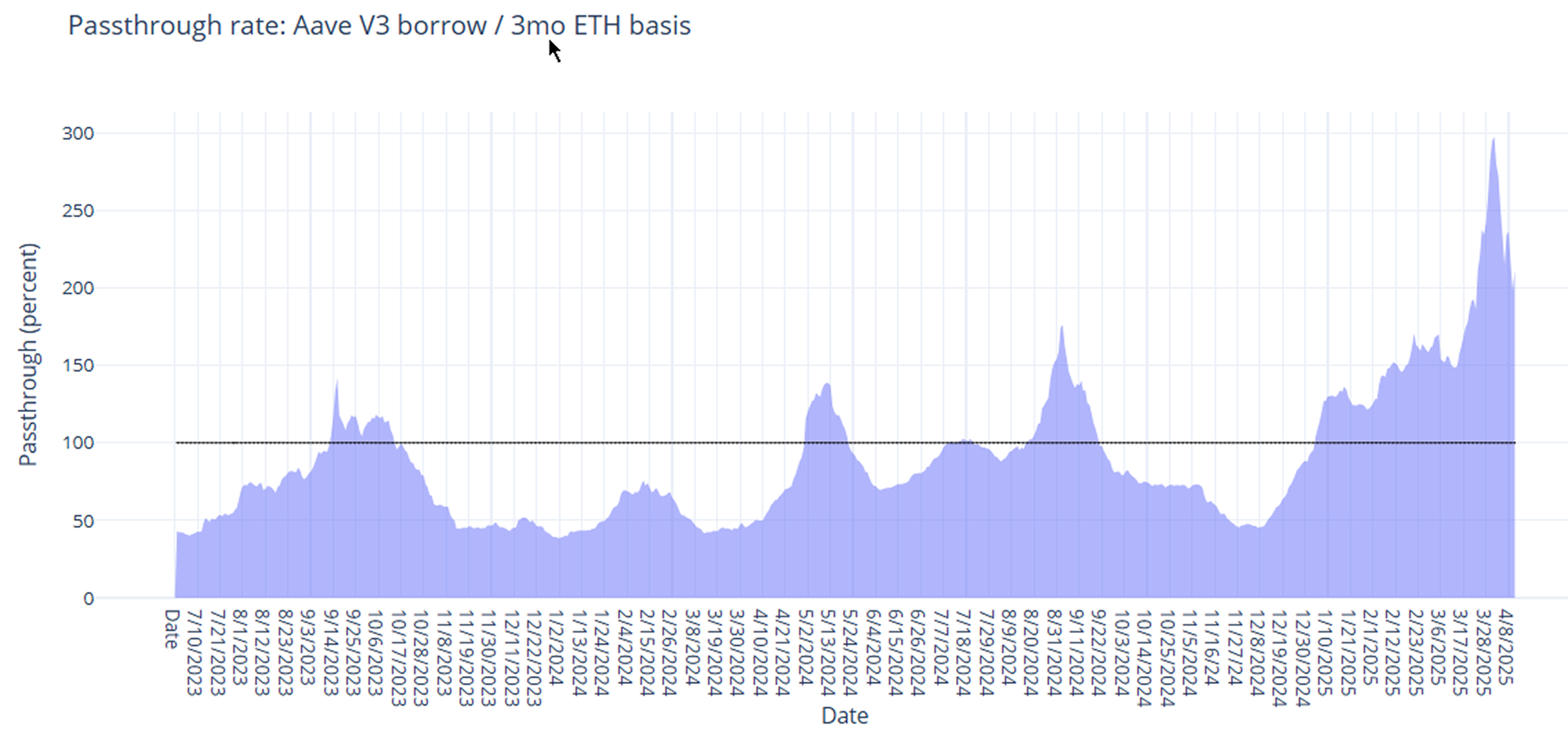

In derivatives markets, funding rates were mixed, with 3-month basis falling by -56bps to 4.57% and perpetual funding rates rising by 25bps to 2.22% on a 30-day trailing basis.

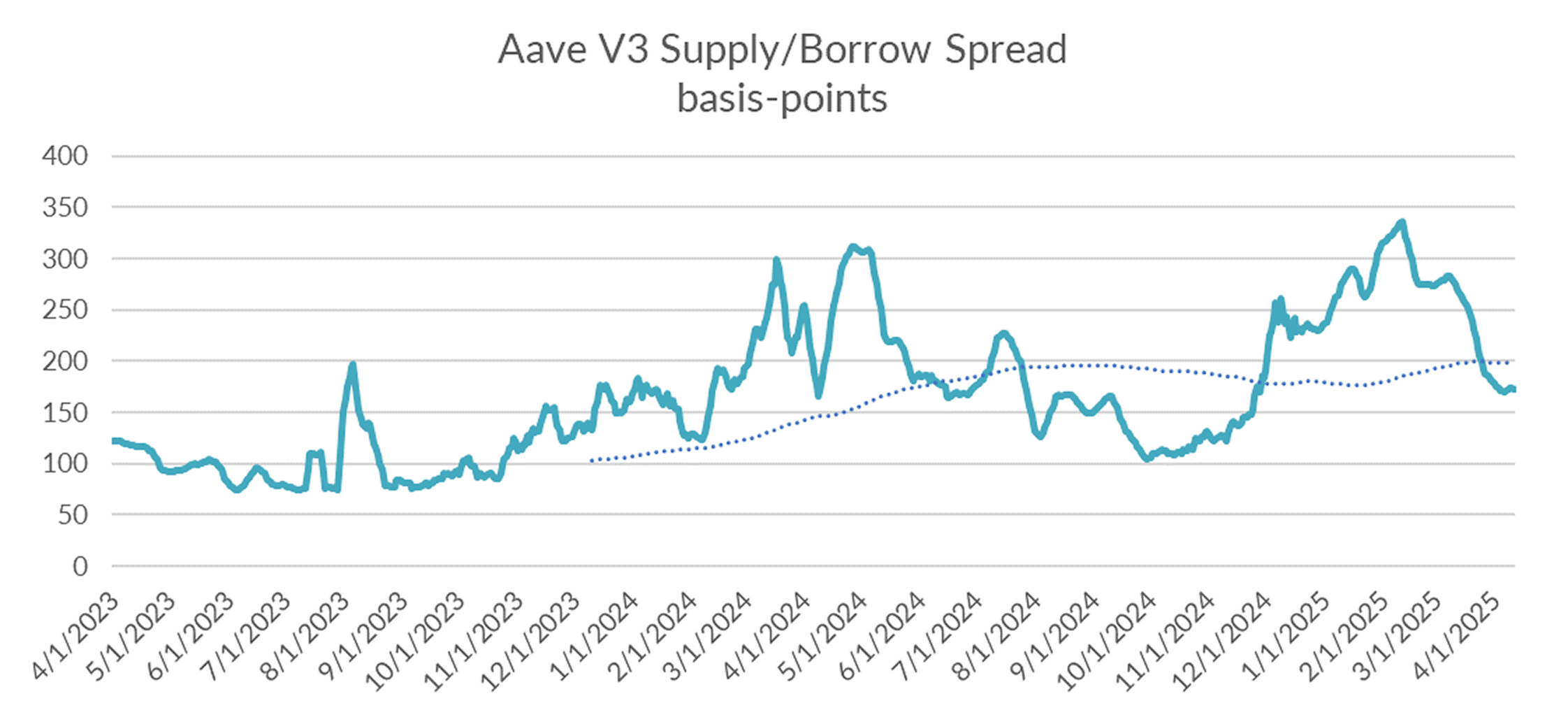

DeFi protocols, on the other hand, held steady, keeping the spread between DeFi rates and derivative rates at historical wides, though the bounce in perp rates helped narrow the spread.

With crypto markets whipsawing on the back of on-again off-again trade tariffs, its hard to pick out the signal from the noise in perp markets but keep an eye on 3-month basis. The trend is still very much in favor of lower rates.

Turning to DeFi variable rate markets, the 30-day trailing average declined another -27bps on the week to 4.69%. Over a shorter lookback period (just seven days), Aave borrow rates averaged 4.50% on the week, foreshadowing continued weakness ahead.

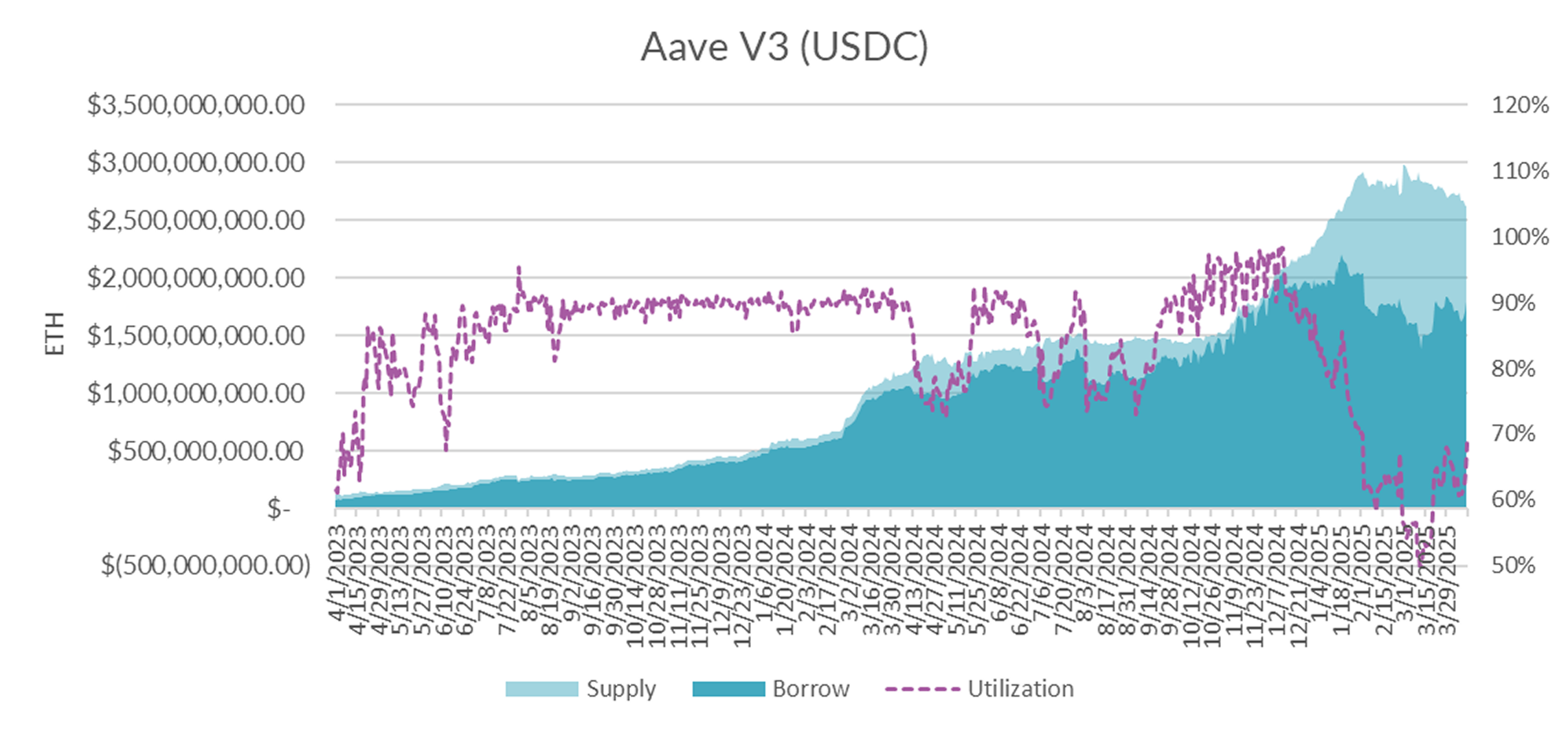

Diving in the microstructure of Aave USDC markets, utilization rose to 69% up from 63% the week prior, due to a combination of declining supply and increased borrow demand (-100M supply, +86M demand).

At 69% percent utilization, this represents the highest rate since early Feb and is a sign of potential stabilization of DeFi yields ahead.

Expect supply rates to pick up and the supply/borrow spread to narrow should this trend continue in the coming weeks.

If utilization can increase on the largest risk market selloff since COVID, that may portend healthier markets ahead.

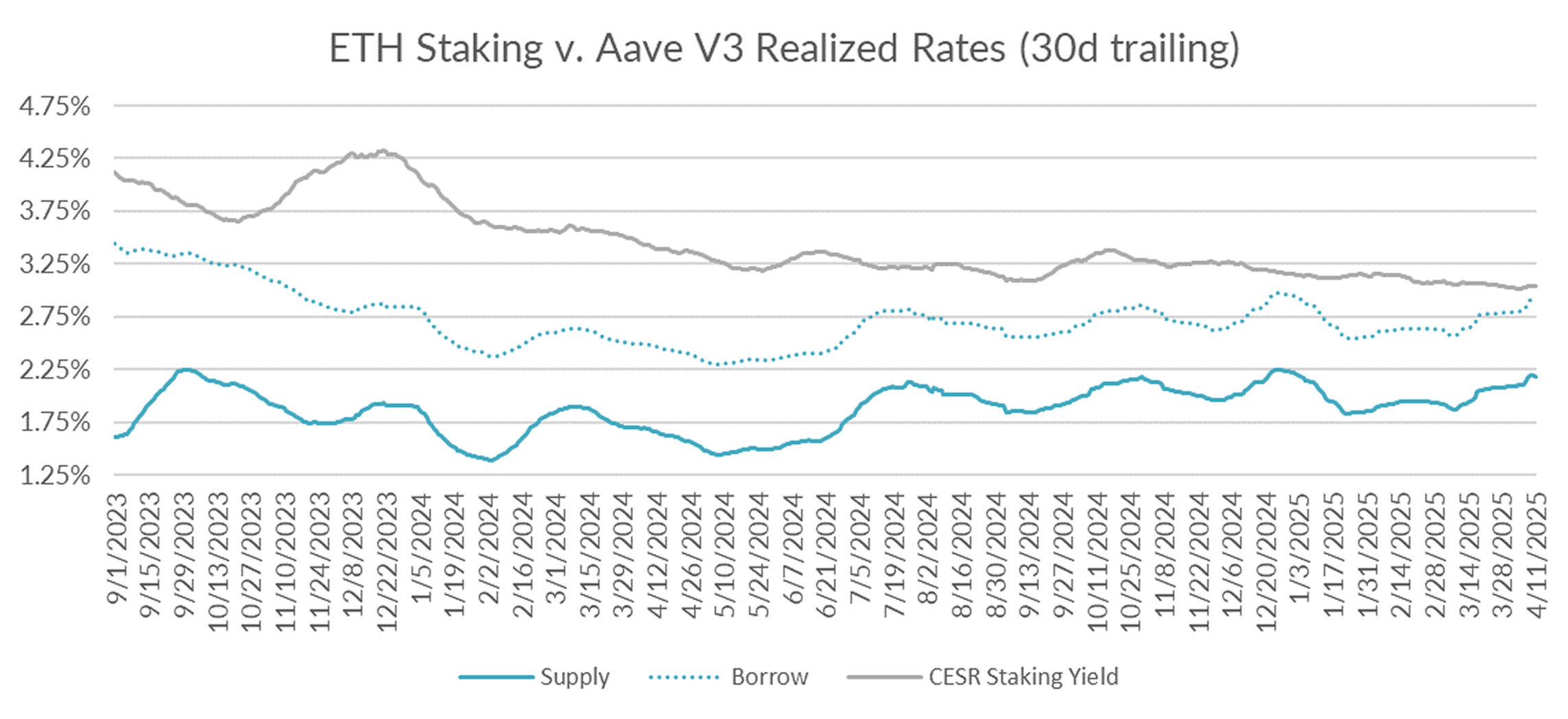

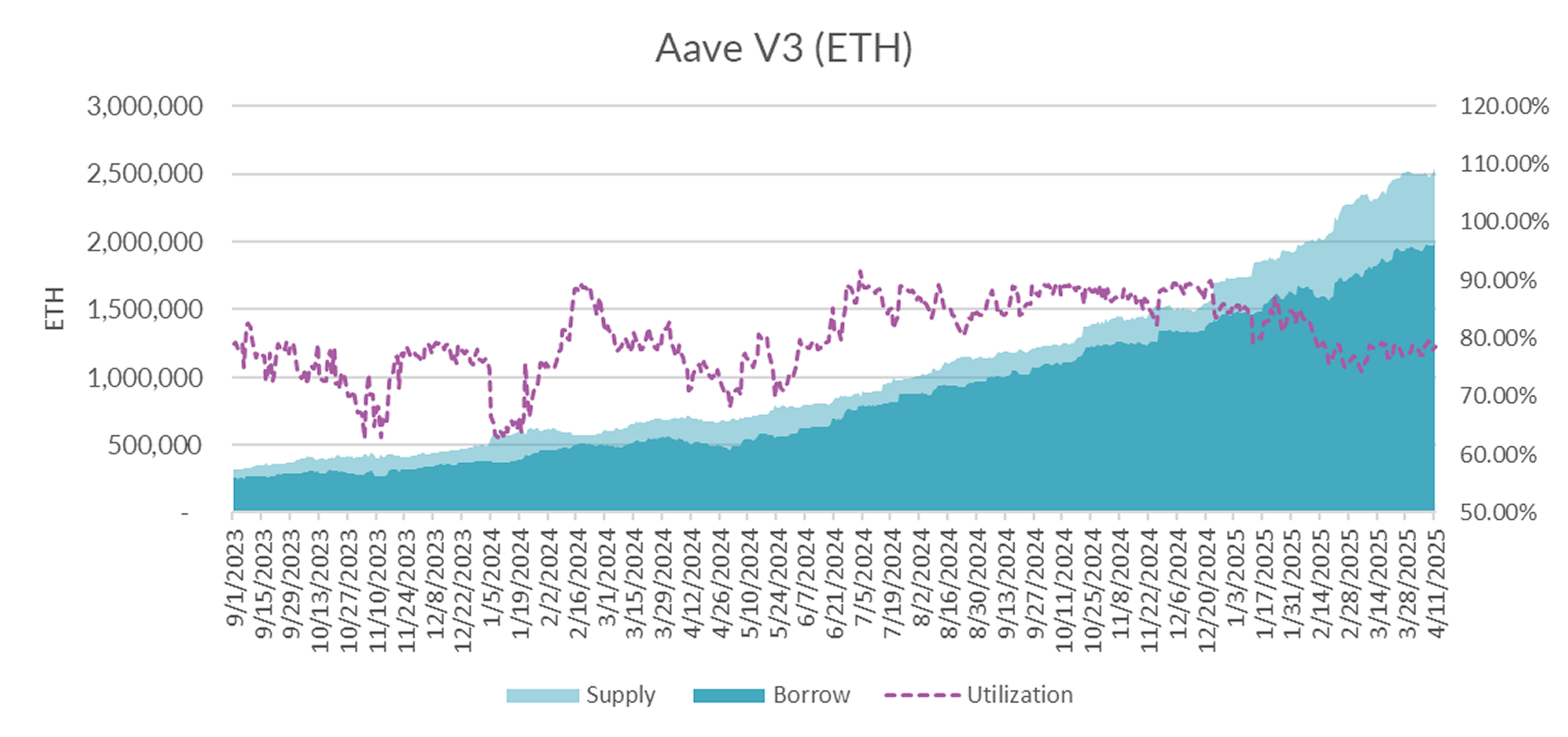

Turning now to ETH markets, ETH rates continue to grind higher, rising by +9bp on the week to 2.89% on a 30-day trailing basis. The CESR staking index also rose, albeit at a slower pace, by just +3bp to 3.04%, causing the spread to narrow by a full -6bps on a 30-day trailing basis.

Market internals show that borrow demand (+72k ETH) outstripped supply (+46k ETH) week on week.

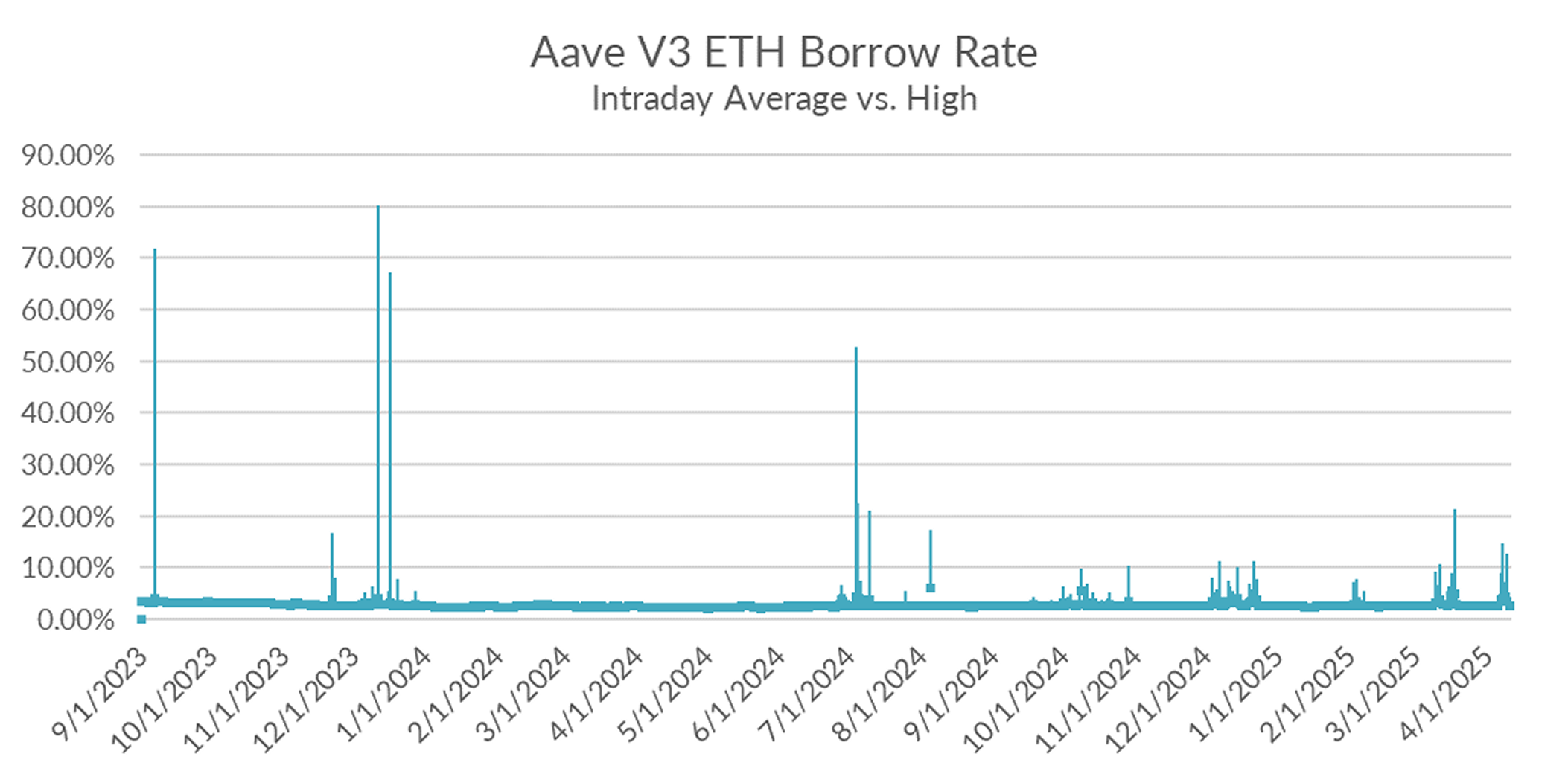

And while overall utilization remains steady in the high 70s, intraday charts show significant stress in the supply/demand picture throughout the week, with borrow rates peaking as high as 11.49% on Tuesday.

Anectdotal evidence suggests that these spikes are short-term hedging flows related to levered short ETH ETF rebalancing needs.

With the announcement of a 90-day reprieve for all trading partners (ex-China), the market stabilized on the week with the S&P 500 up ~9.28% off the lows. Bitcoin closed the week unchanged after outperforming the week prior, showing resilience in a volatile macro environment. With Bitcoin unable to meaningfully decline in a market that is preparing to digest the largest trade tariffs in nearly a century, it seems any good news from here should be highly positive for the asset. With the dollar index DXY on the precipice of breaking a major level ~100, investors may begin to see BTC as the safe haven asset that it promises to be. For lending markets, this means potentially higher rates ahead.