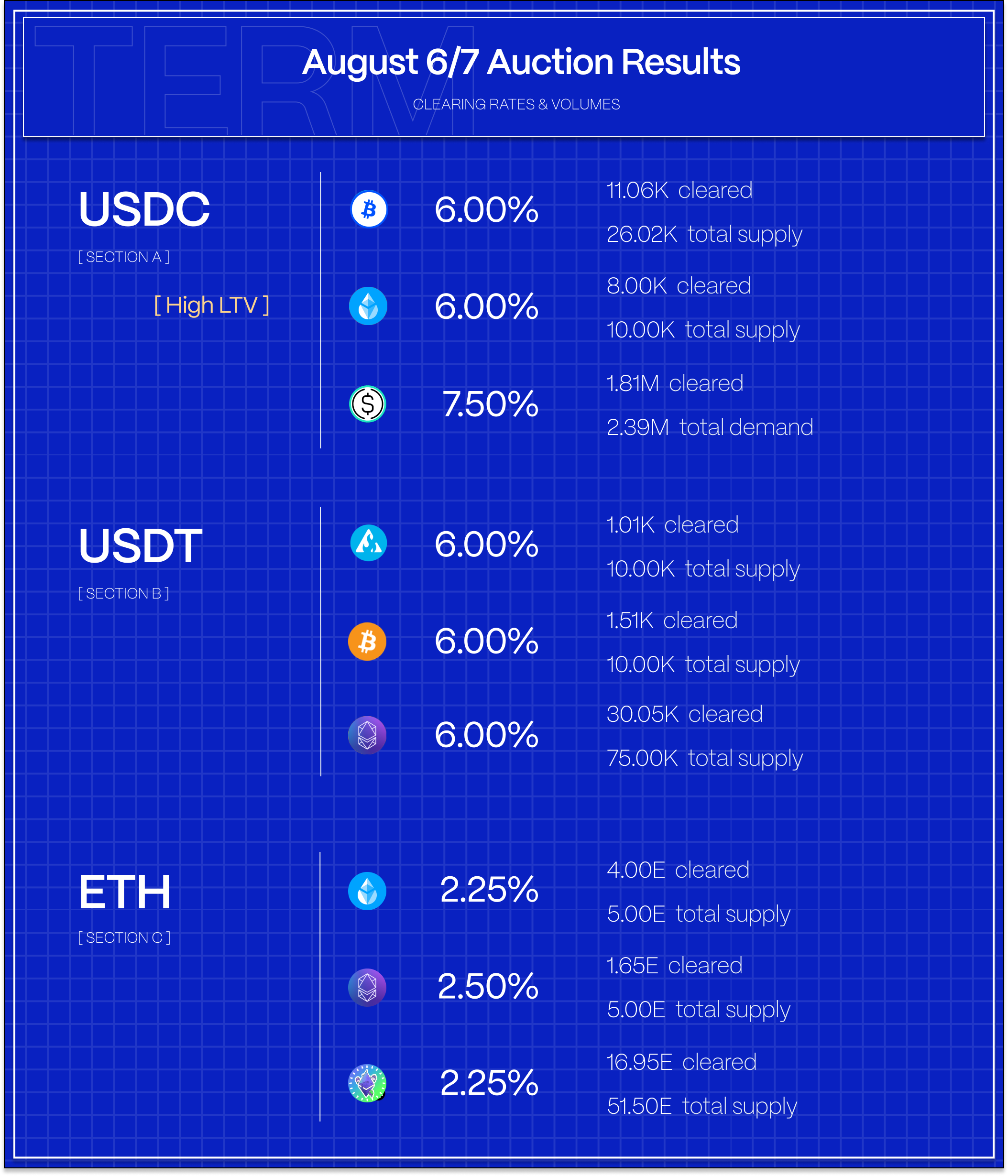

Matched maturity July PT-sUSDE loans rolled off last week leading to a short dip in loans outstanding as borrowers prepared to re-establish their looping positions. A total of $1.8M cleared at 7.50% this week against the Sep PTs versus $2.4M of demand. In ETH markets, demand to borrow against pufETH saw good traction on the integration of Term finance markets into the vePUFFER gauge (currently offer 100% APY in incentives to borrowers).

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

Basis and Perpetuals Markets

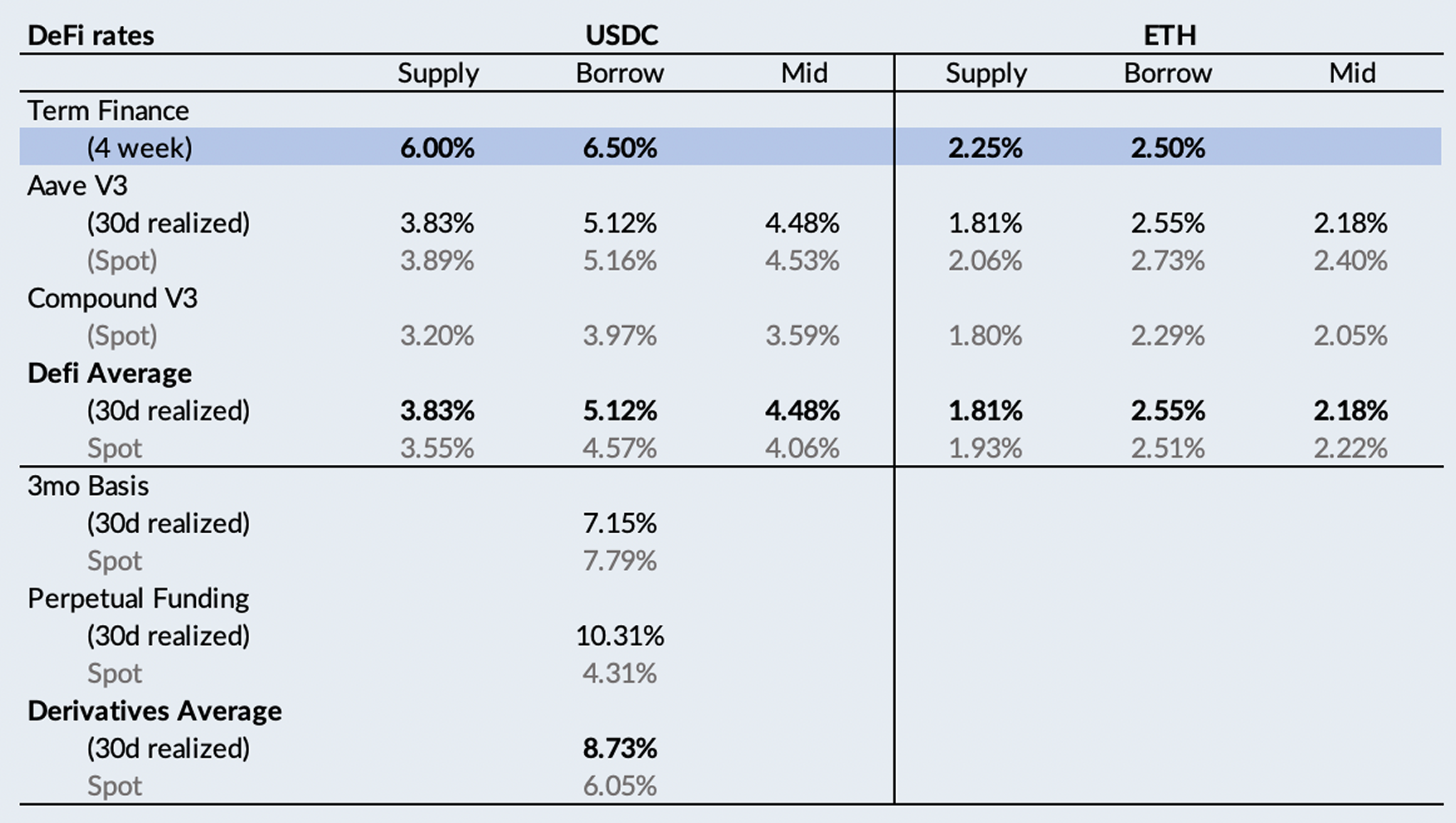

In derivatives markets, funding rates declined slightly, consistent with sideways BTC price action throughout the week. On a 30-day trailing basis, 3-month basis rose +55bps to 7.15% and perpetual funding rates closed the week at 10.31%, down -19bps from the week prior. On a shorter lookback, perpetual funding rates averaged just 4.59%, suggesting declines ahead.

DeFi rates, on the other hand, have been relatively stable, causing the spread between DeFi and derivatives to stabilize

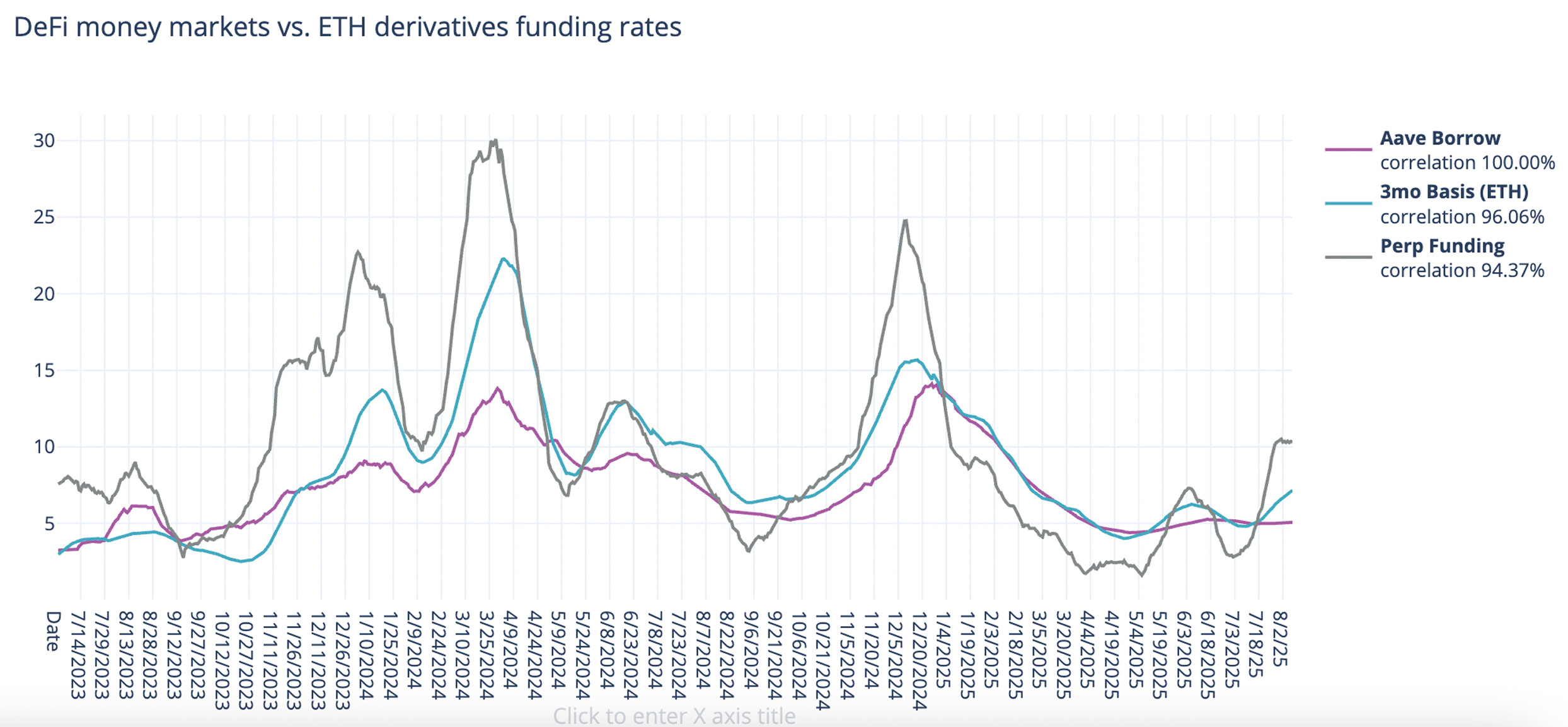

The divergence between 3-month basis and perp rates is, perhaps, not surprising when taking the growth in Ethena tvl over the past two weeks into account. Since July 14, Ethena tvl has increased from 5.3B to 9.8B, +4.5B in a short manner of time (Ethena dashboard). This rapid increase in balance sheet with which to fund perp leverage in crypto is bringing more stability to perp rates but also cannibalizing the yield. With balance sheet with which to fund perp leverage +4.5B in just two weeks and risk appetite for leverage beginning to taper with BTC trading in a narrow range,, rates are expected to fluctuate sideways in the near term.

USDC Markets

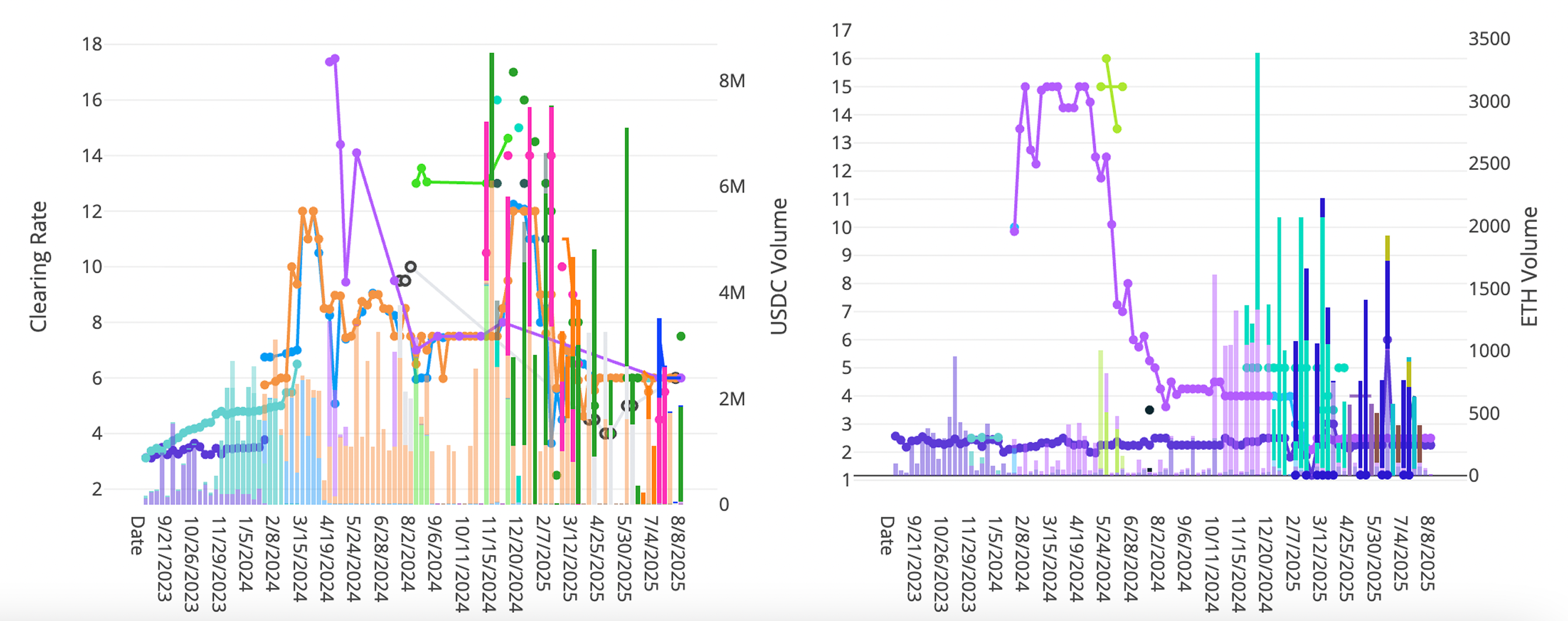

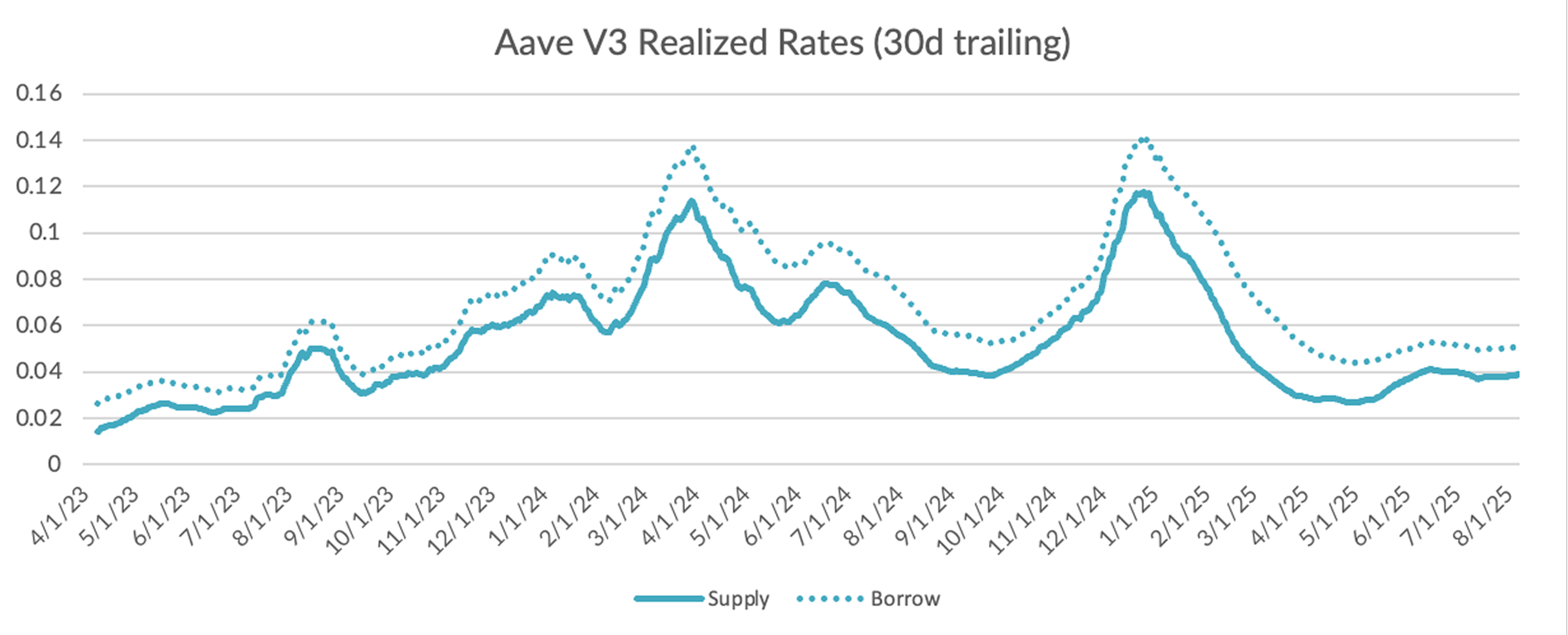

Turning to DeFi variable rate markets, the 30-day trailing average closed roughly unchanged, rising by just +4bps on the week to 5.07% .

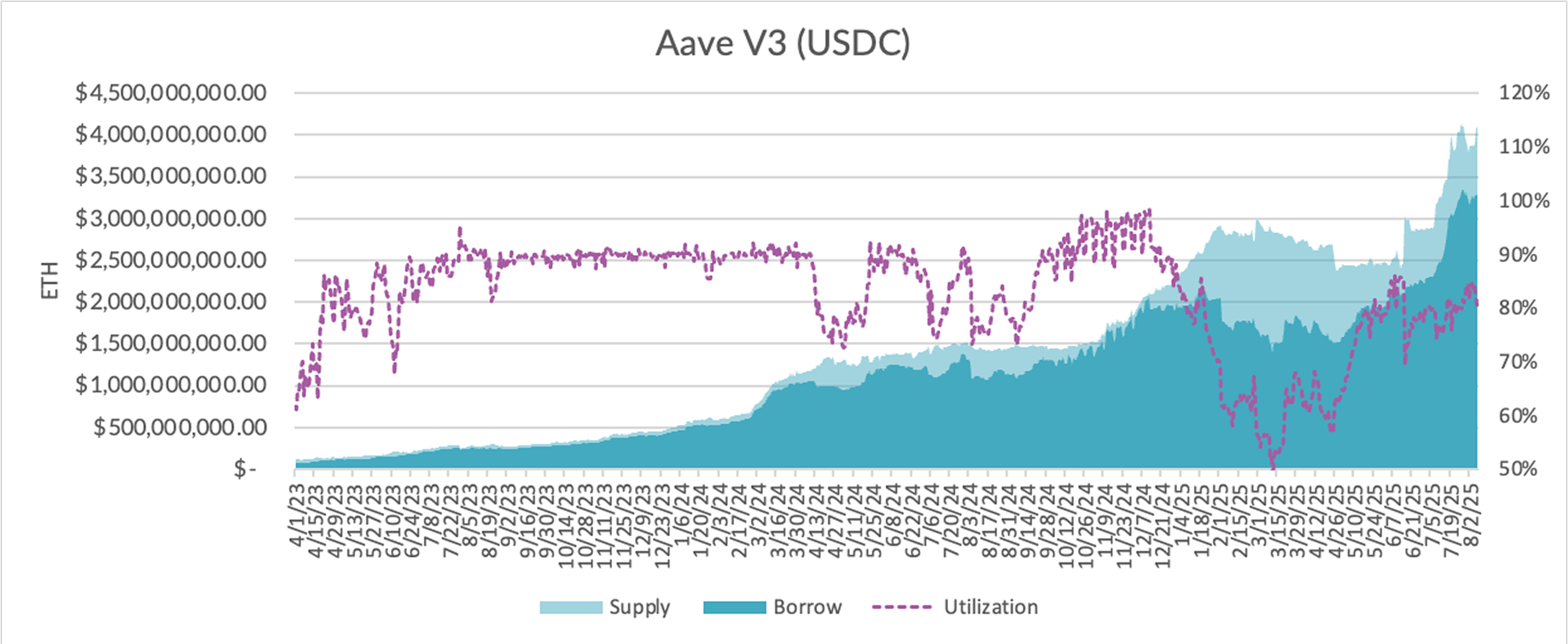

Diving into the microstructure of Aave's USDC markets, utilization held steady in the low-eights, with supply outpacing borrow demand significantly (+300M supply vs. +75M demand).

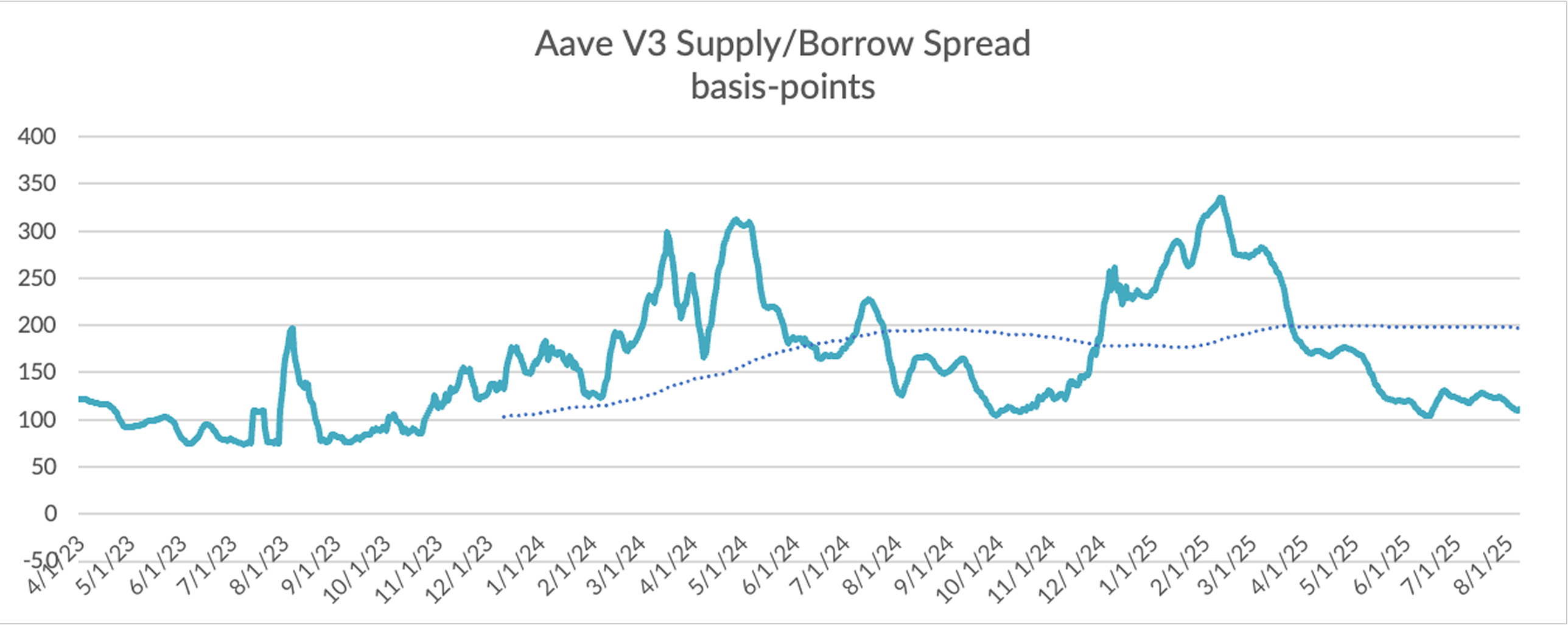

With the overall market relatively balanced, borrow-supply spreads remain near the low end of the range.

And while demand stands near all time highs, total supply continues to maintain pace.

USDC markets appear relatively balanced but with perp rates beginning to taper and Aave supply continue to increase at a rapid rate, expect rates to continue sideways if not lower.

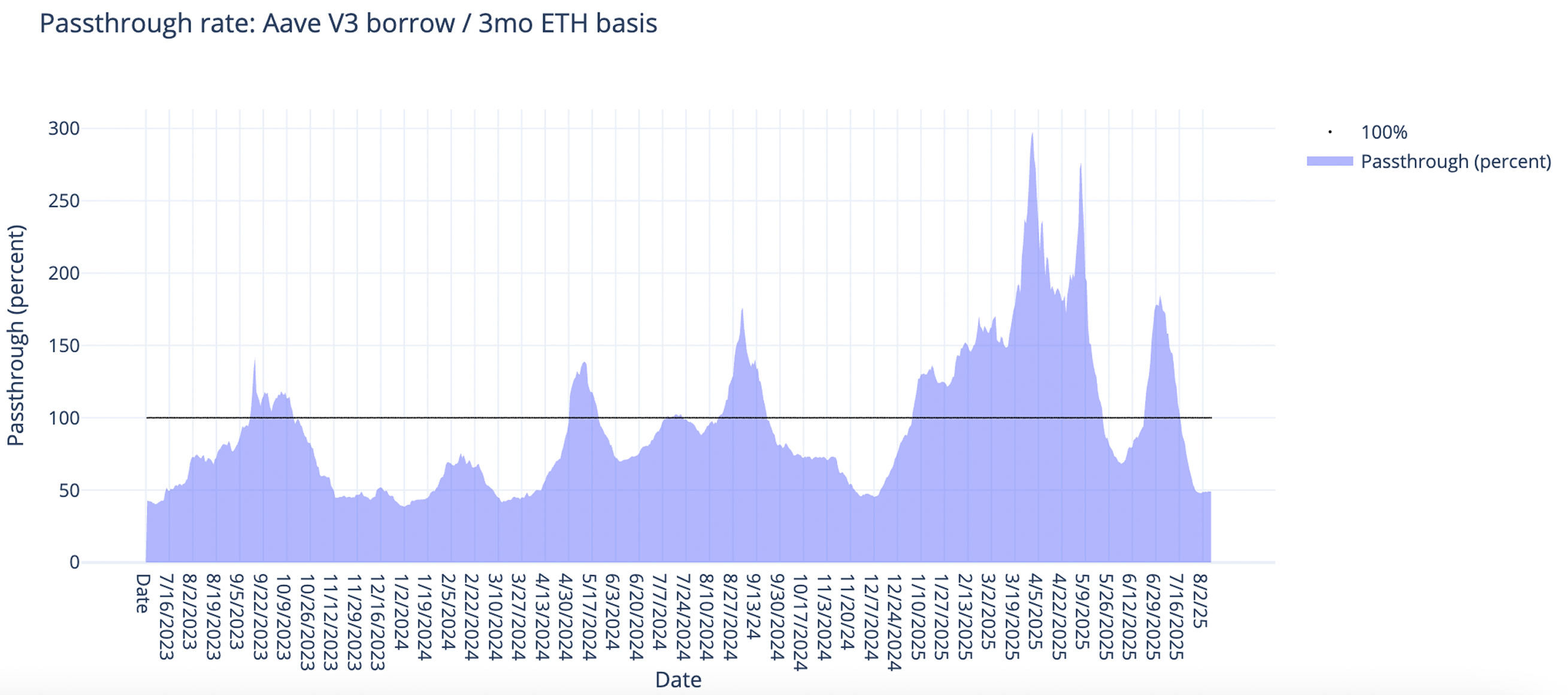

ETH Markets

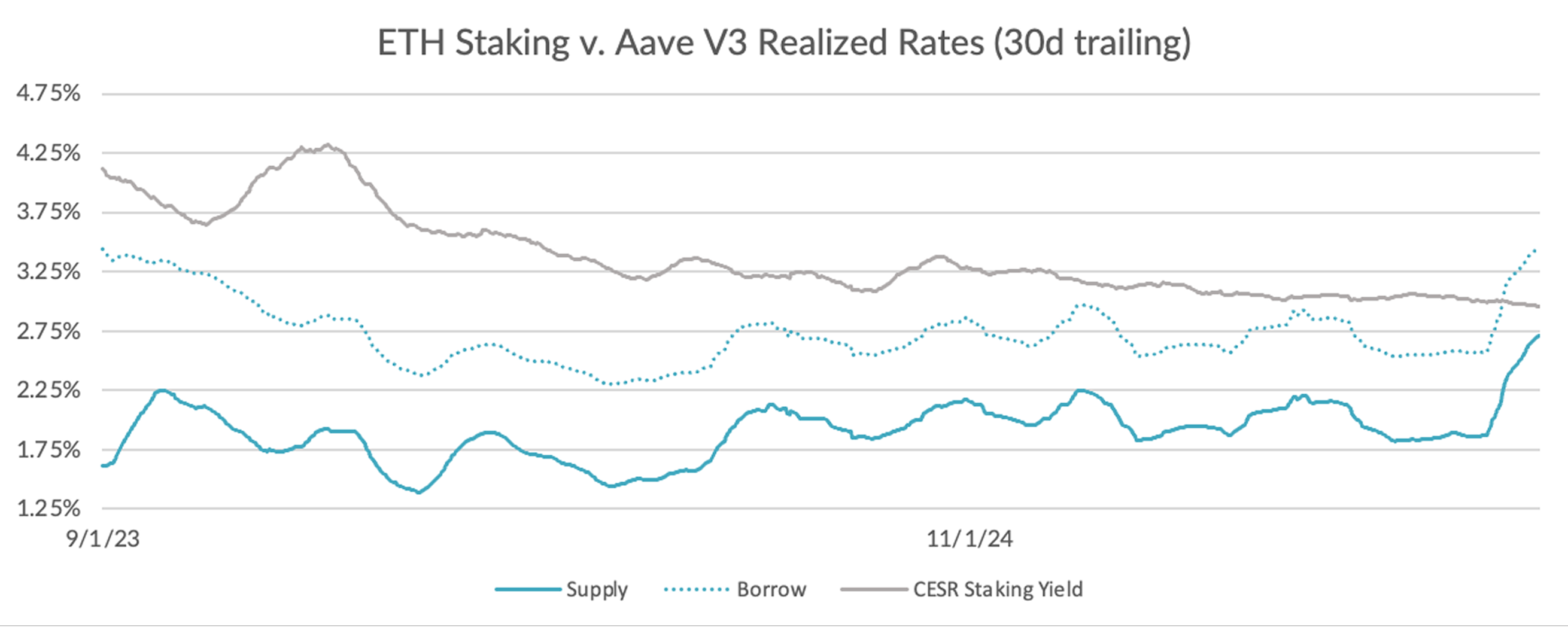

Turning now to ETH markets, ETH rates rose +11bps to 3.44% on a 30-day trailing basis, in large part due to the sharp spike in ETH rates a couple weeks ago. The CESR staking index, on the other hand, fell -2bps to just 2.95% on a 30-day trailing basis, causing the spread to invert for the first time in the past two to three years.

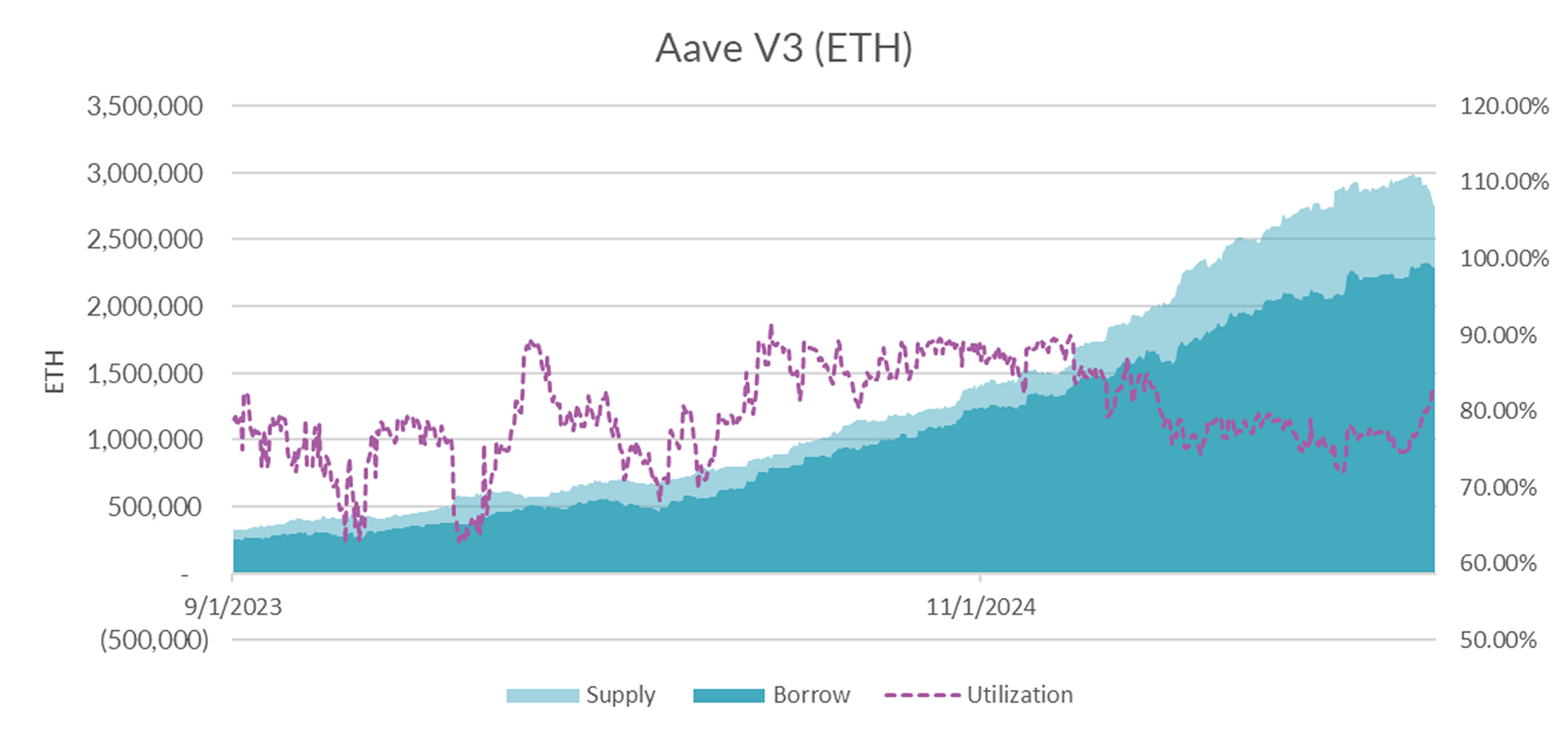

Market internals show that Aave has reversed the sharp decline in ETH supply late last month only in part. At 2.7M ETH, supply remains -273K off historical total ETH supply highs seen early July.

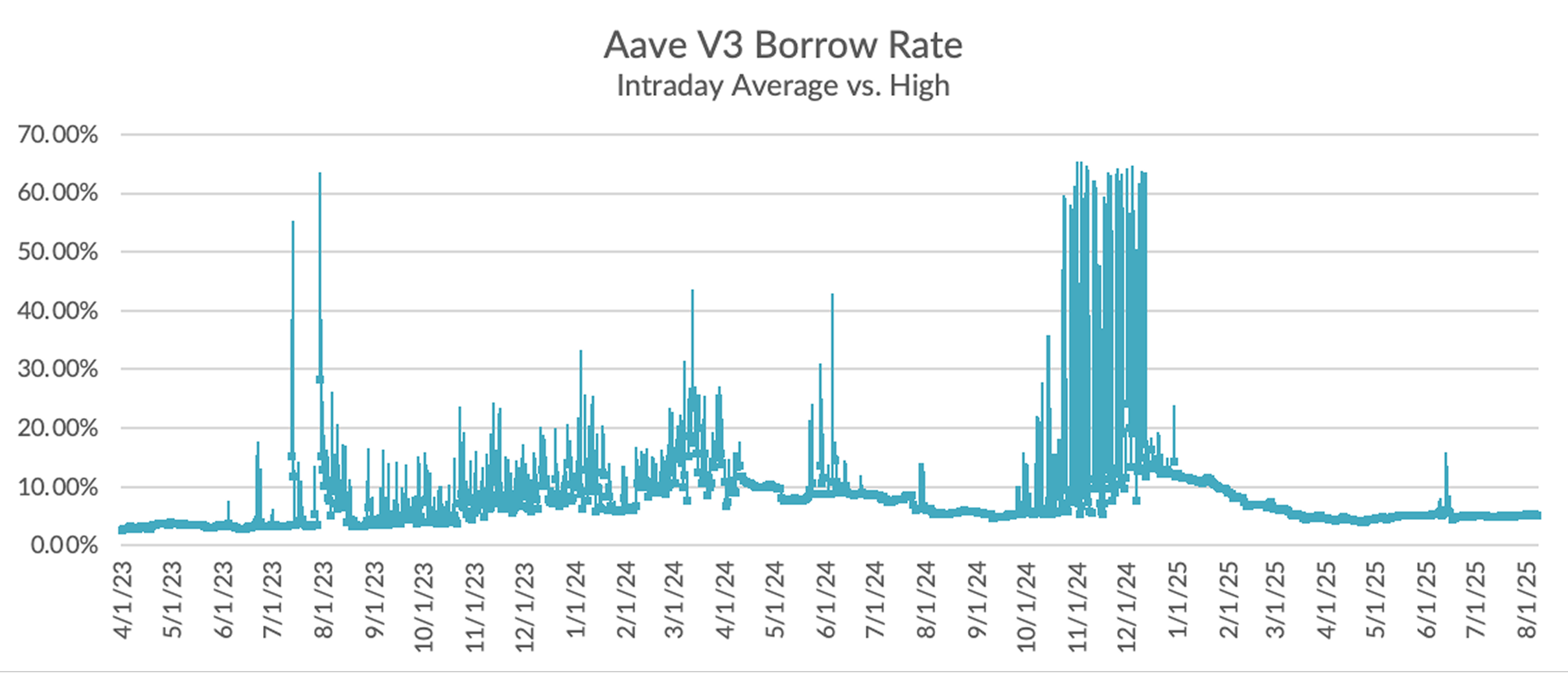

Diving into the intraday charts, we see that ETH borrow rates have been well behaved in recent weeks.

With ETH staking rates solidly below 3% and ETH borrow rates beginning to heat up, it will be interesting to see how LST/LRT tvl is impacted over the medium term.

The ‘animal spirits’ of the ETH community is beginning to pick up with ETH outperforming BTC handily week on week (+2.85% vs. +16.26% for ETH). This narrative is boosted by recent developments in U.S. regulatory clarity via passing of the Genius act that promises to increase stablecoin adoption in the U.S. Nevertheless, 3-month basis remains steady in the 6-7% range and perp rates are declining sharply due, in part, to Ethena’s rapidly increasing balance sheet. Aave USDC market exhibit a similar trend of suppressed DeFi rates, given its seemingly endless supply of below market USDC liquidity. One theory is that DeFi has long enjoyed elevated yields driven by a “risk premium” for operating in a niche, early-stage market. As stablecoins gain broader adoption and mainstream participants grow more comfortable allocating to DeFi, this premium may compress—ushering in a new era of tighter spreads and structurally lower yields.