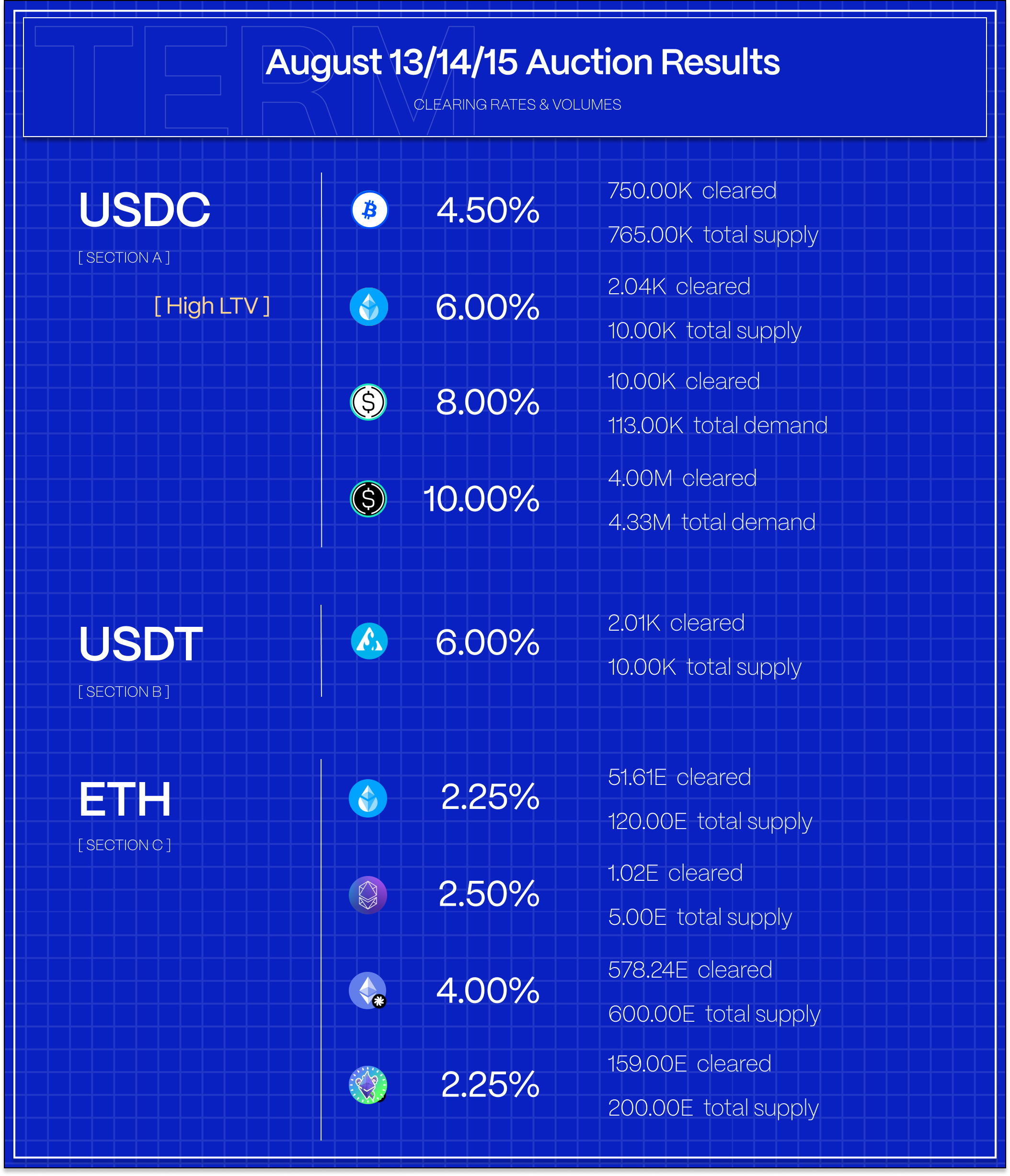

Matched maturity Sep PT-sUSDE borrows onboarded in earnest this week with the PT-USDe variant offering the best yields — around $4M cleared at 10%. In ETH markets, demand to borrow against pufETH continues to see growth with the integration of Term finance markets into the vePUFFER gauge, while superETH borrows continue to roll.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

In derivatives markets, funding rates resumed to the upside with ETH briefly touching all time highs intraweek. On a 30-day trailing basis, 3-month basis rose +48bps to 7.62% and perpetual funding rates closed the week at 10.41%, up +11bps from the week prior.

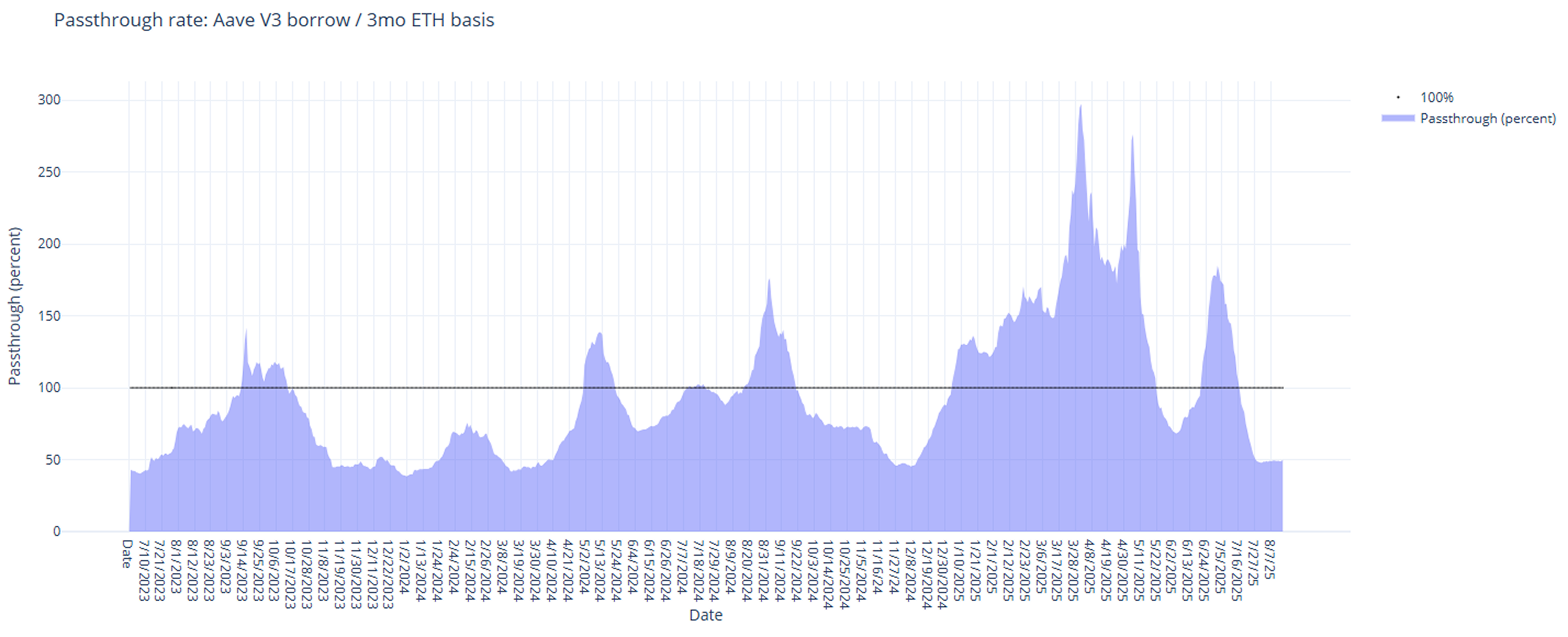

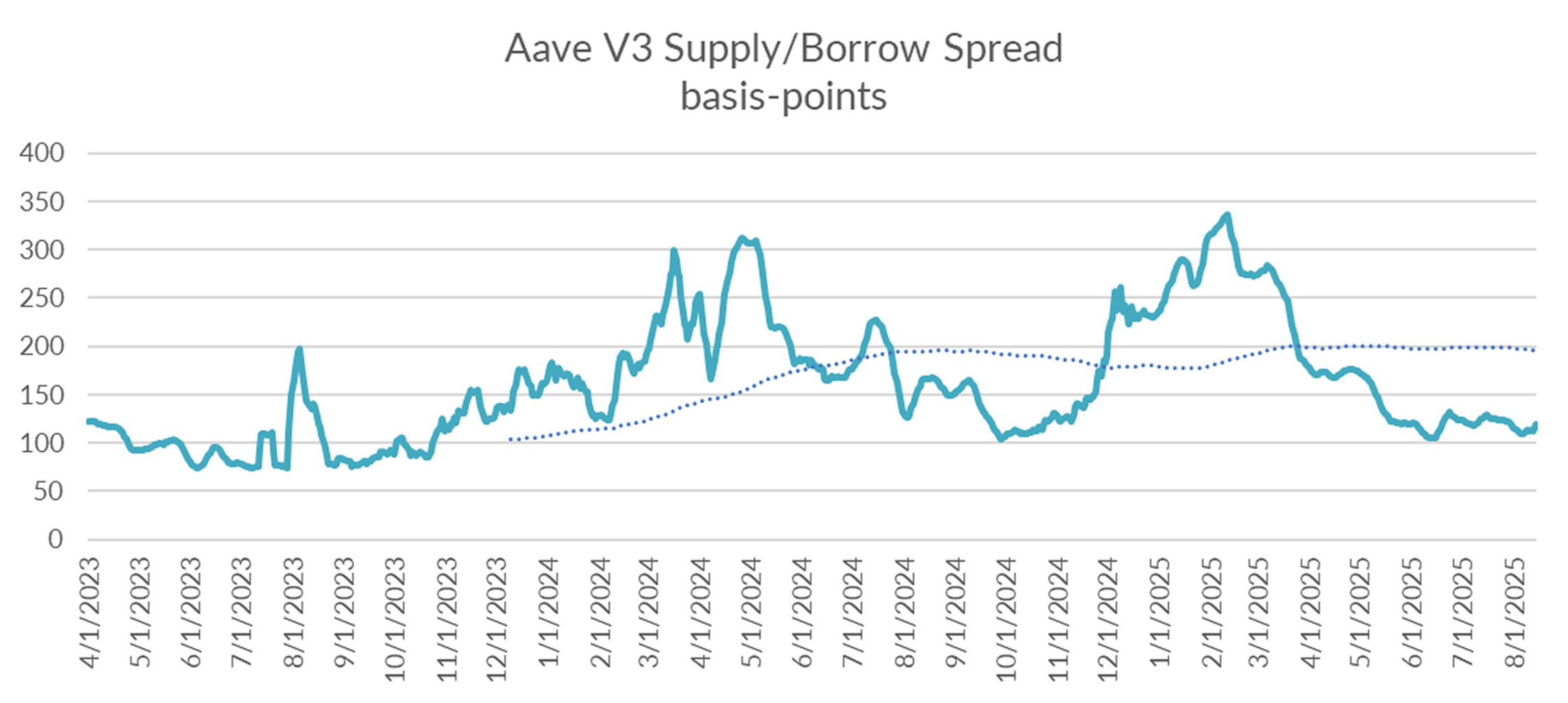

DeFi rates are starting to move to the upside but remains well below derivatives funding rates and continues to sit near the low end of its historical range relative to perp rates.

The dip in perpetual funding rates last week was short-lived. Bullish sentiment continues to buoy funding rates and the rising tide is finally beginning to filter through to DeFi borrow rates.

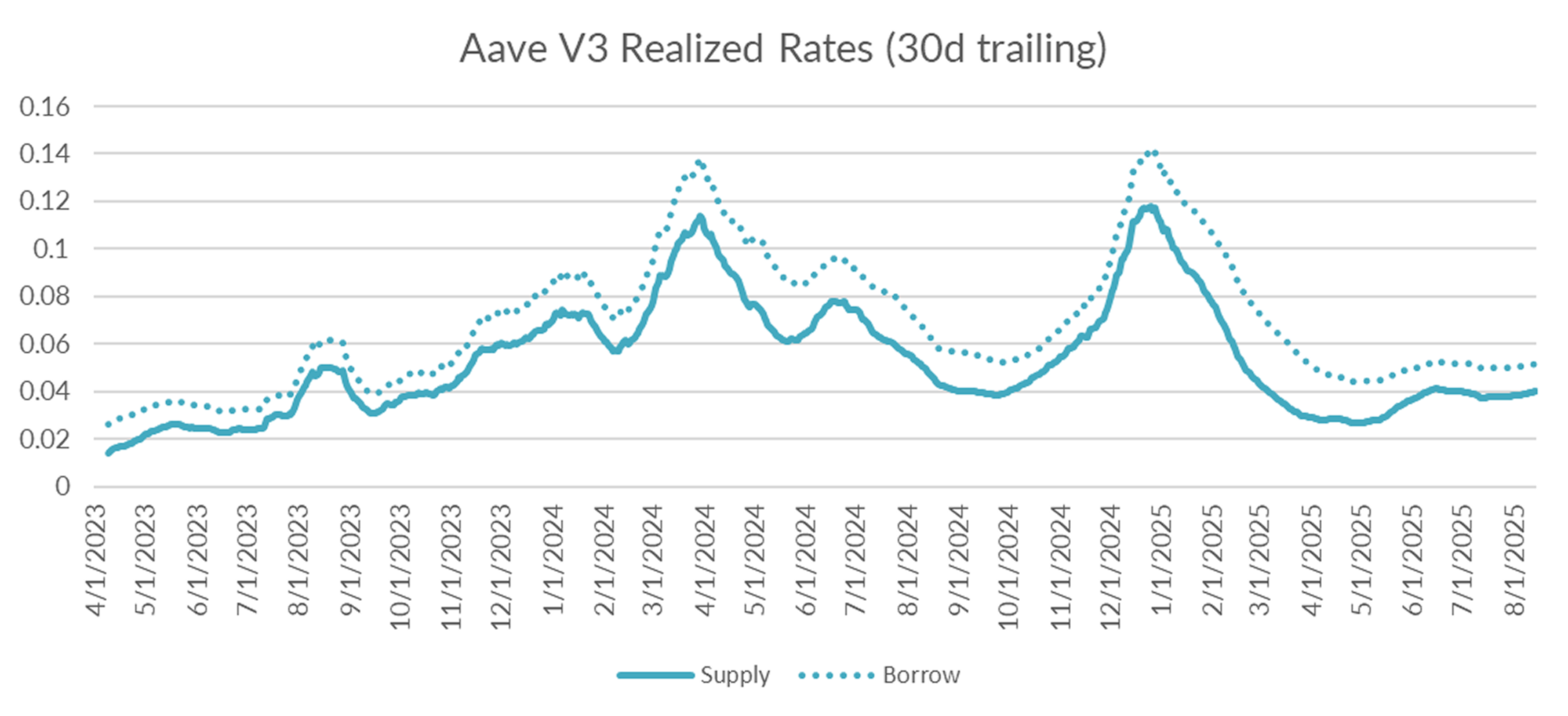

Turning to DeFi variable rate markets, the 30-day trailing average rose +11bps to close at 5.19% on a 30-day trailing basis. On a shorter lookback period, USDC borrow rates averaged 5.35% suggesting further gains ahead.

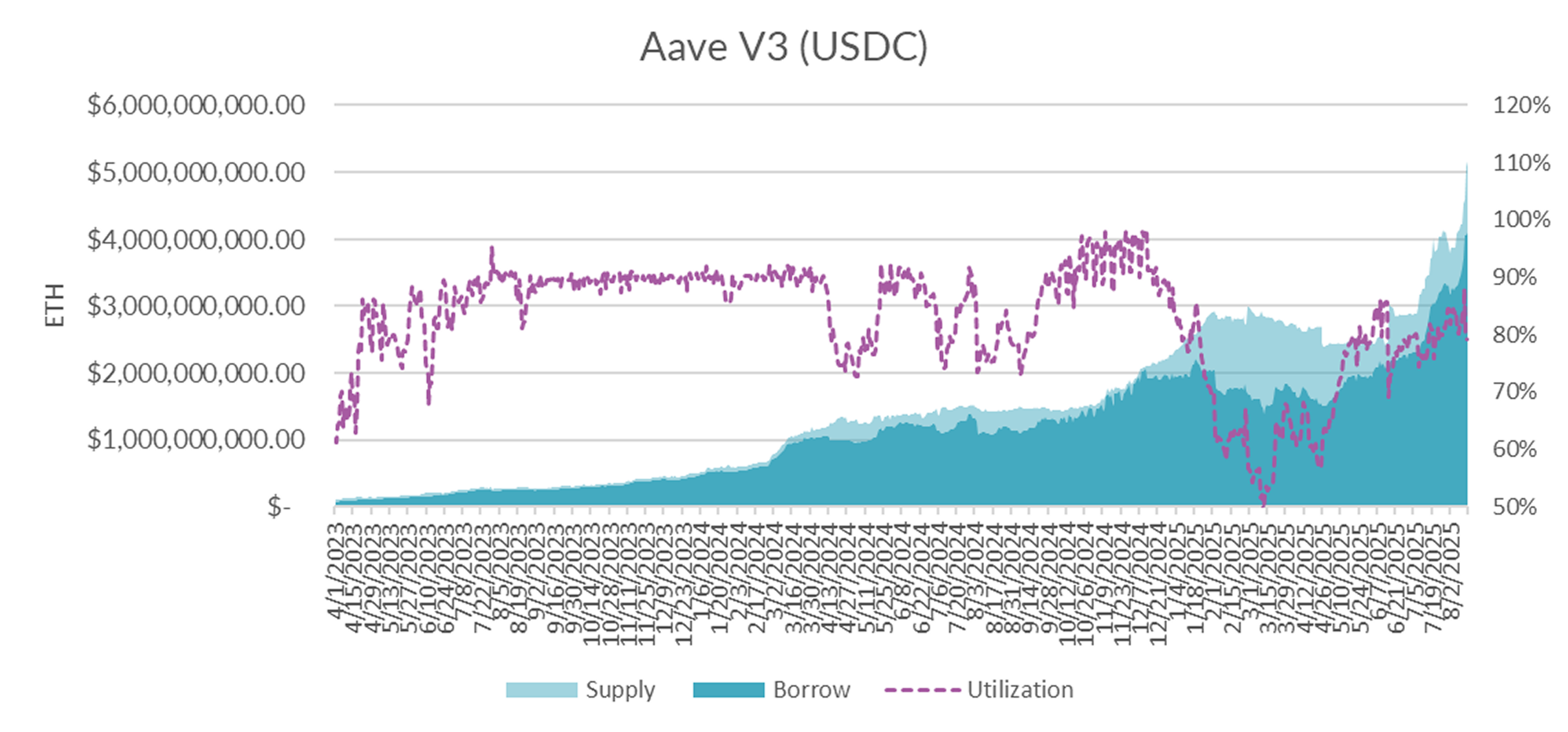

Diving into the microstructure of Aave's USDC markets, both supply and borrows rose sharply over the past week (+1BN supply vs. +790M demand), as if coordinated, keeping utilization steady at 80%.

With the overall market relatively balanced, borrow-supply spreads remain near the low end of the range.

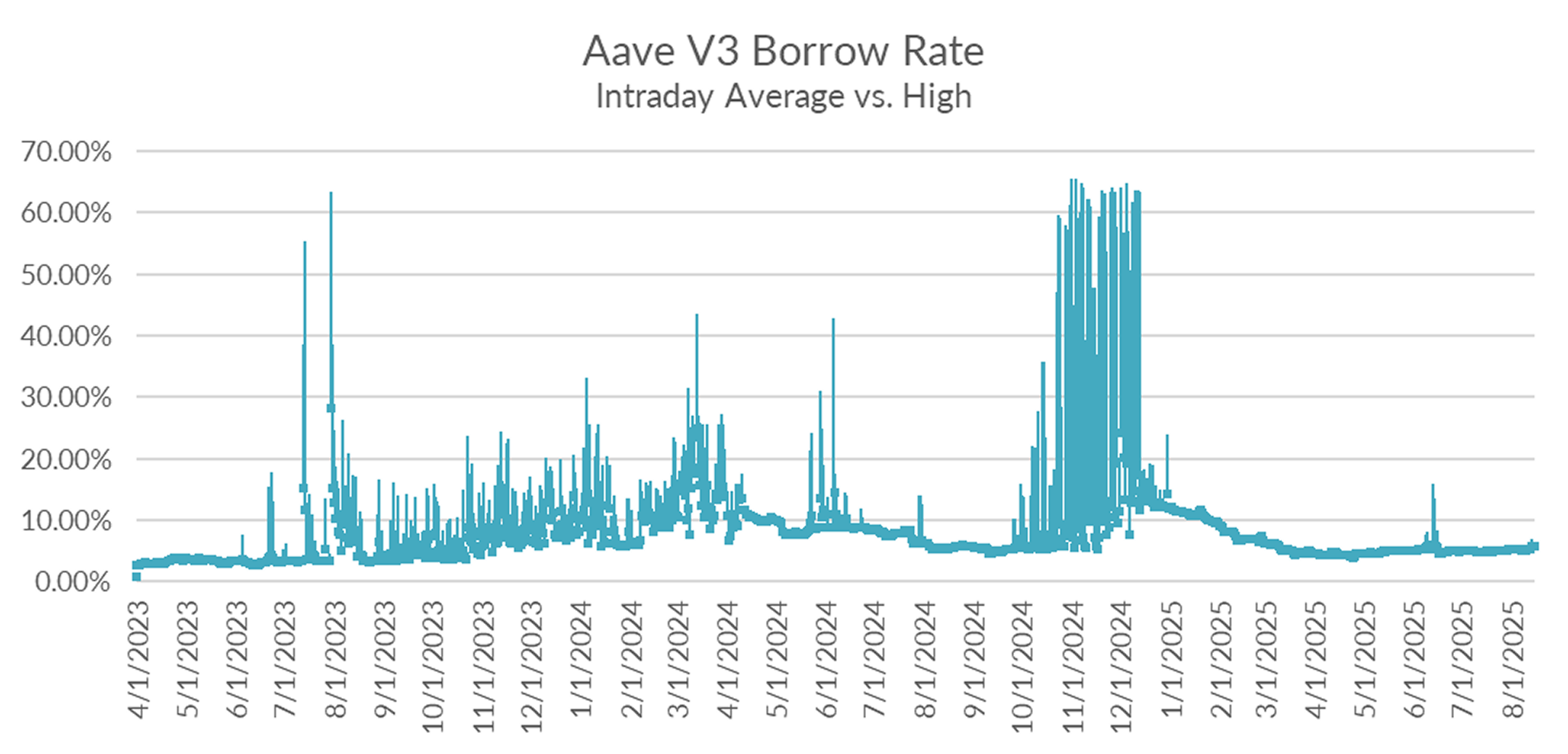

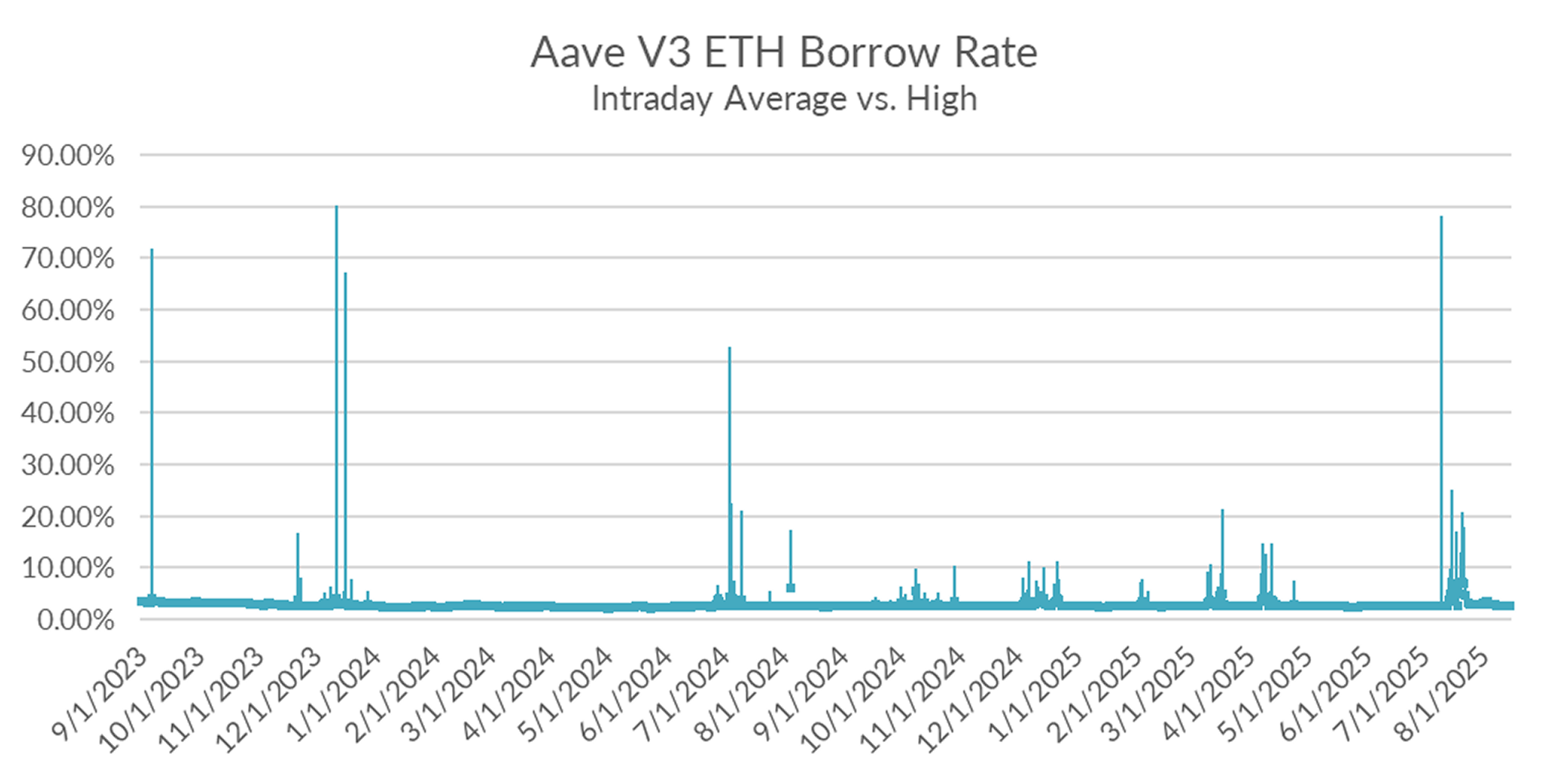

Intraday spikes through the kink are beginning to occur with increasing frequency, but not yet to the point where it registers on historical charts.

With the overall depth of Aave increasing at a rapid rate, expect the frequency of large and sudden spikes to decline and rates to remain muted in the near and medium term, absent large withdrawals (like those often attributed to Justin Sun). For reference, the last time Aave saw an extended period of 60%+ intraday rates, USDC Supply stood at just ~1.5BN. As of time of writing, it stands around 6BN.

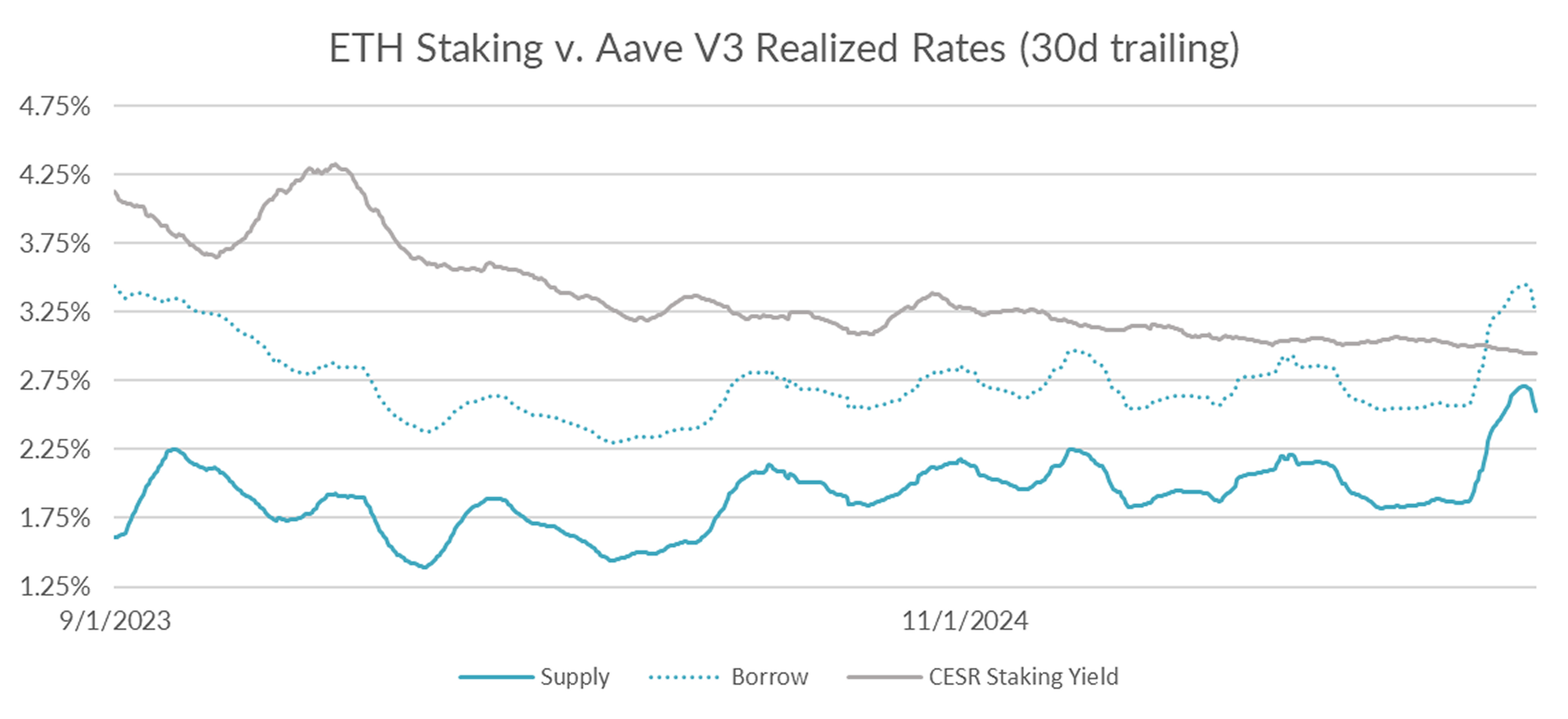

Turning now to ETH markets, ETH rates fell -21bps to 3.24% on a 30-day trailing basis, normalizing as the 150K ETH withdrawal from a few weeks ago begins to roll out the lookback window. The CESR staking index, on the other hand, remains steady at 2.94%, falling just -1bp on a 30-day trailing basis, keeping the spread inverted for the time being.

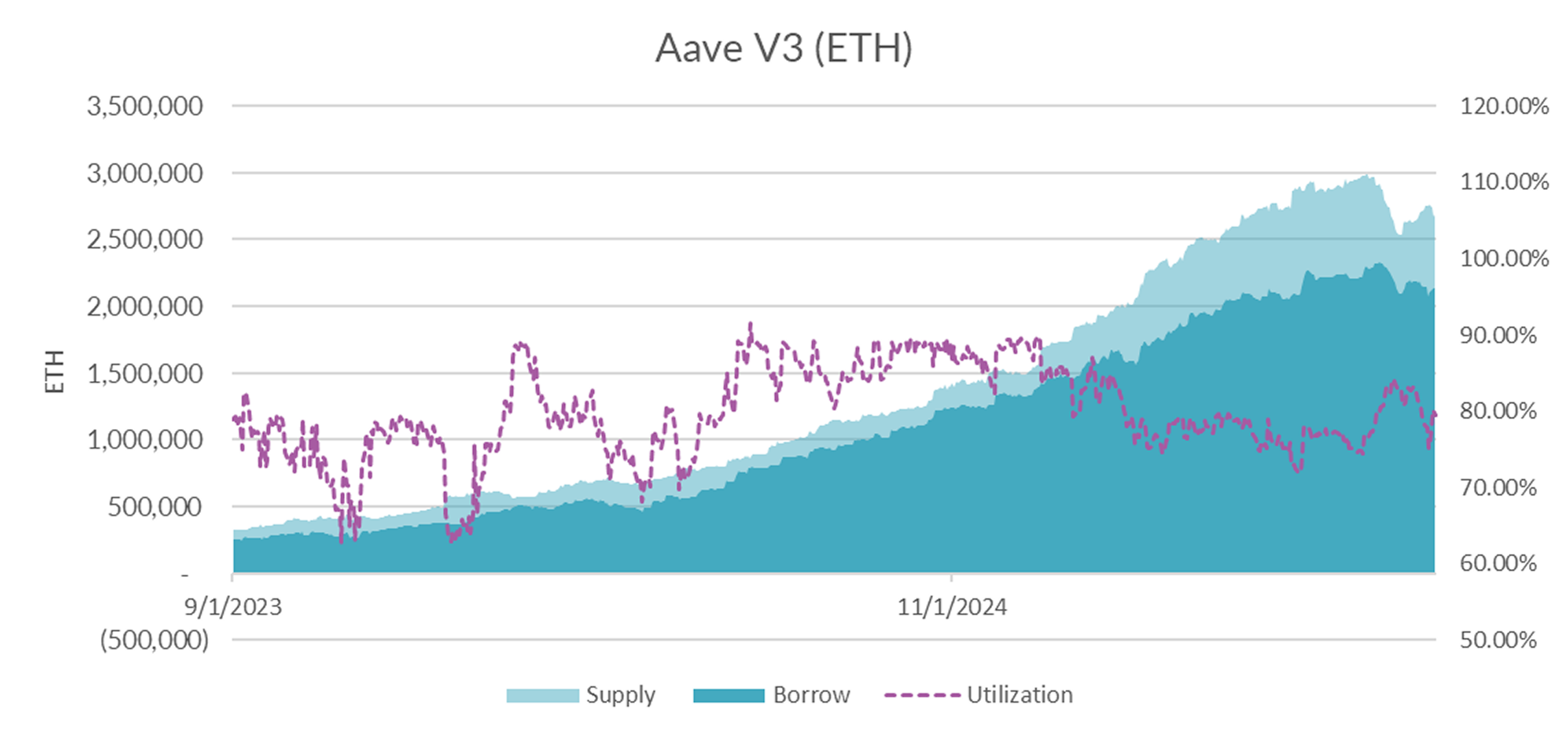

Unlike USDC markets, which appear to be a one-way train higher, market internals on ETH show that supply may be topping out. At 2.7M ETH, supply remains -273K off historical total ETH supply highs seen early July.

Diving into the intraday charts, we see that ETH borrow rates have been well behaved in recent weeks, further supporting the normalization after the 150K ETH withdrawal incident from a few weeks ago.

Despite recent normalization of rates, the LST/ETH borrow spread continues to remain well below historical averages, even over a shorter one-week lookback (~30bps). This dynamic is beginning to show through Lido’s withdrawal queue, which now stands at 22-days to redemption.

In stablecoin inflows/outflows, the past month has seen massive inflows of about +16BN onchain. These gains were relatively evenly split between USDe, USDT and USDC. This move coincides with the passing of the Genius, which promises to bring much more capital onchain. Overall this is bearish for DeFi rates but extremely bullish for DeFi in the medium to long-term.

Cryptoasset markets, led by ETH, logged another strong week. ETH is up 9.82% at the time of writing, though this figure masks sharp intraweek swings that briefly pushed it back to all-time highs near $4,700. A significantly higher than expected PPI Friday morning (0.9% vs 0.2% expectations) put a damper on asset prices as markets priced in a more hawkish Fed. Expect this correction to be short-lived, however, as a stagflationary environment where growth is low and inflation is high should be constructive for a store of value like Bitcoin.