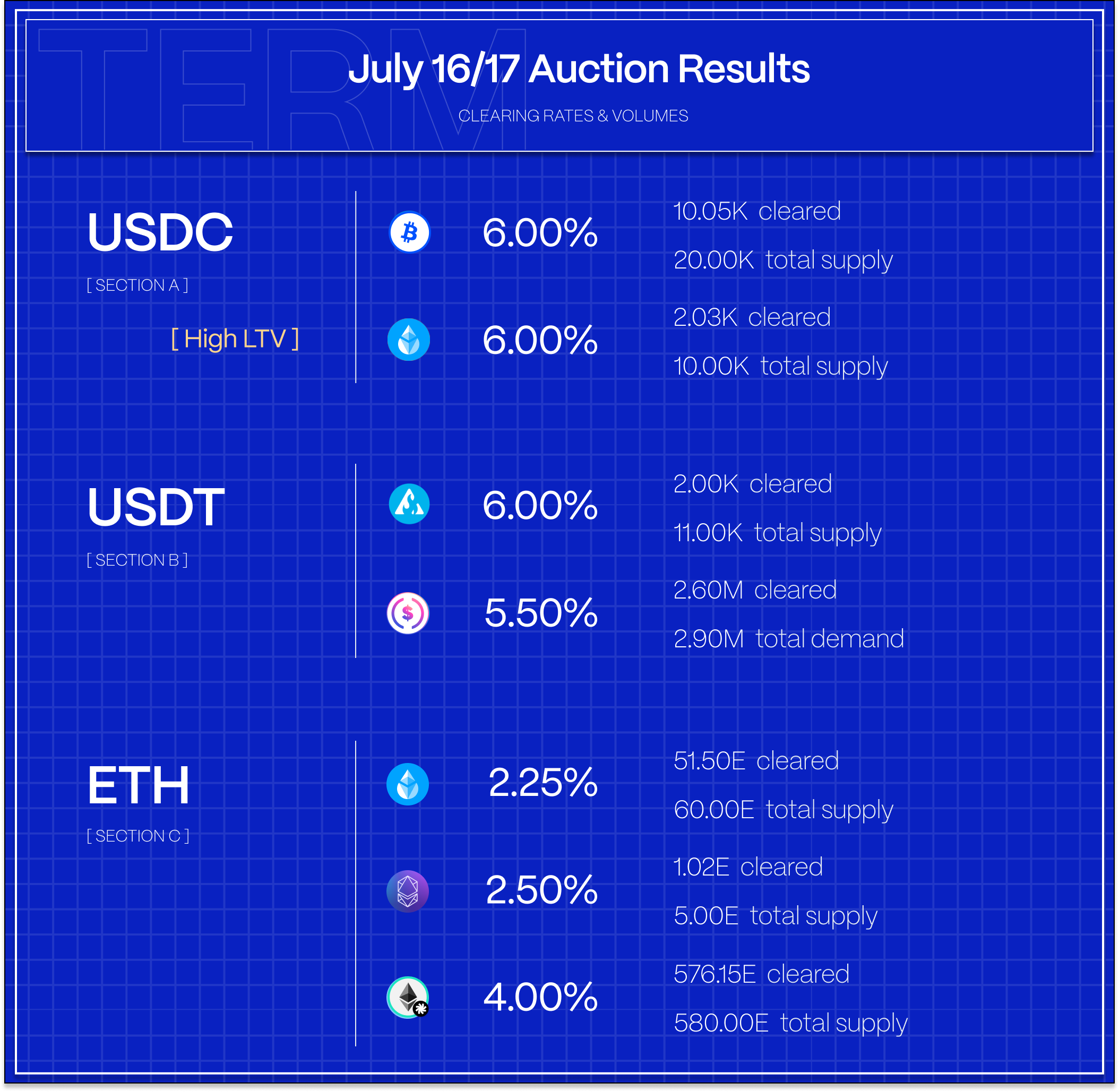

Rates picked up across the board in both USDC and ETH markets even as volumes remained relatively consistent week on week. In USDC markets, volume was driven primarily by USDT loans against deUSD on Avalanche. In ETH markets, demand remains robust against various exotic ETH vault tokens.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

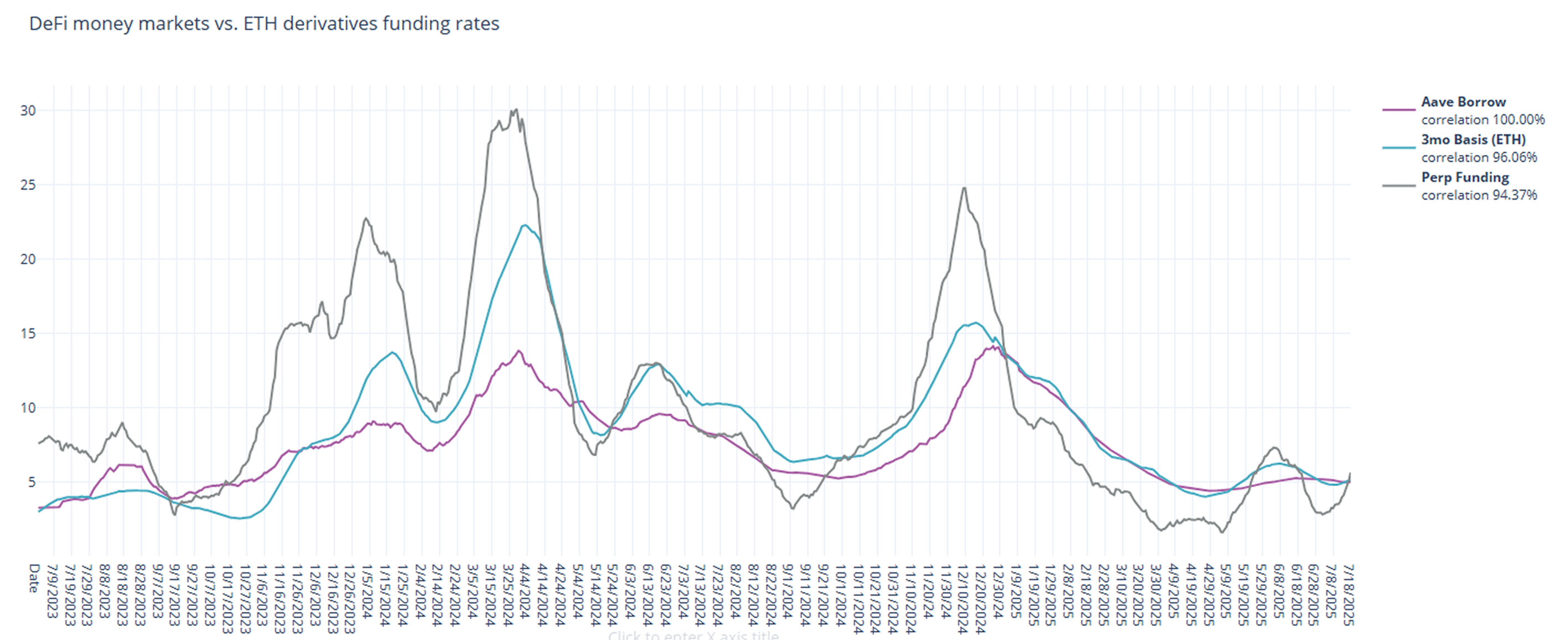

In derivatives markets, funding rates accelerate to the upside, consistent with BTC price action throughout the week. On a 30-day trailing basis, 3-month basis rose 30bps to 5.12% and perpetual funding rates closed the week at 5.62%, up +213bps from the week prior. On a shorter lookback, perpetual funding rates averaged 12.25%, suggesting a potential rate squeeze ahead.

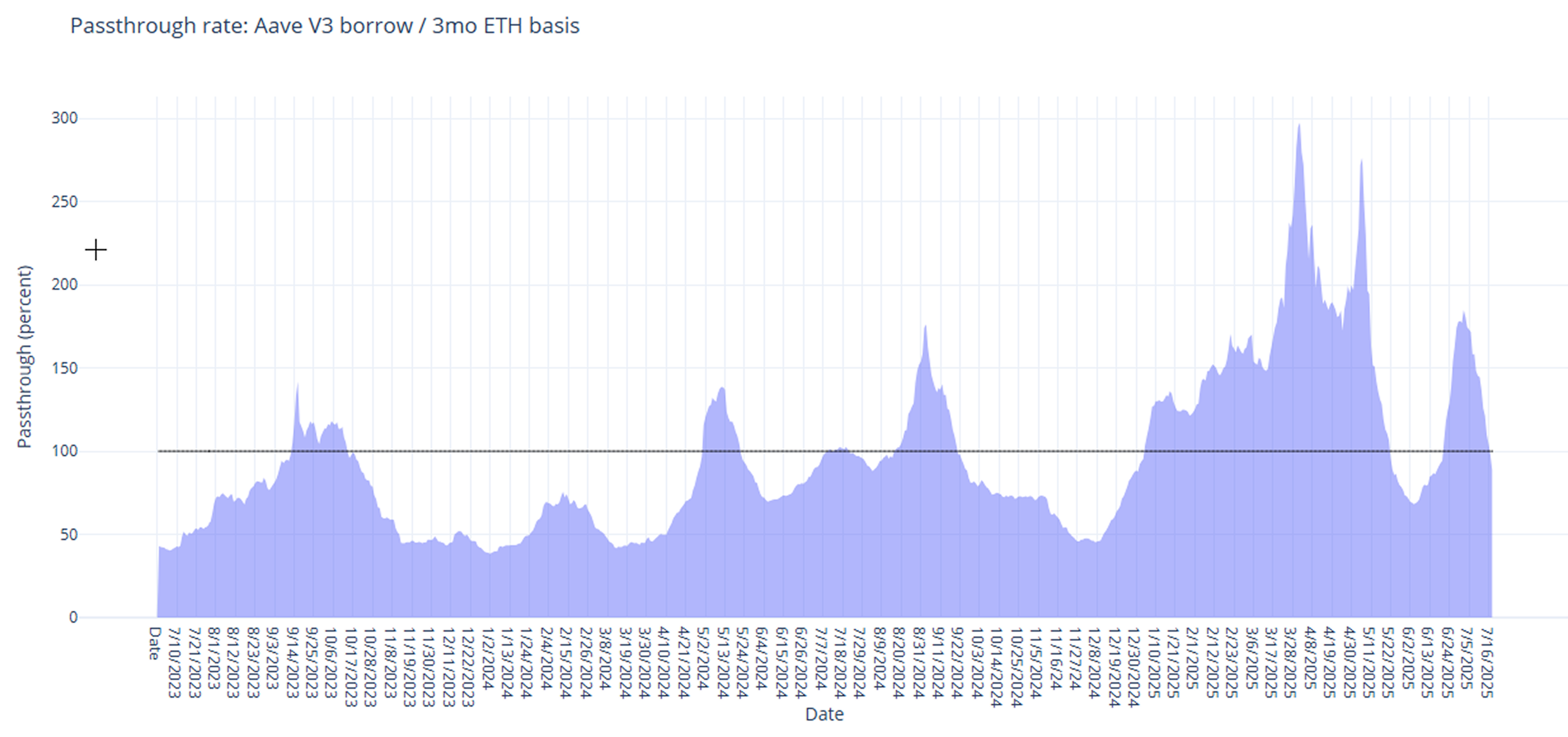

DeFi rates, on the other hand, have been relatively stable, causing the spread between DeFi and derivatives to narrow back toward historical averages.

With BTC and alts breaking through on the follow, risk appetite for leverage is showing staying power. Expect rates to remain elevated in the medium term.

Turning to DeFi variable rate markets, the 30-day trailing average actually fell -5bps on the week to 5.00% despite rapidly rising rates in derivatives.

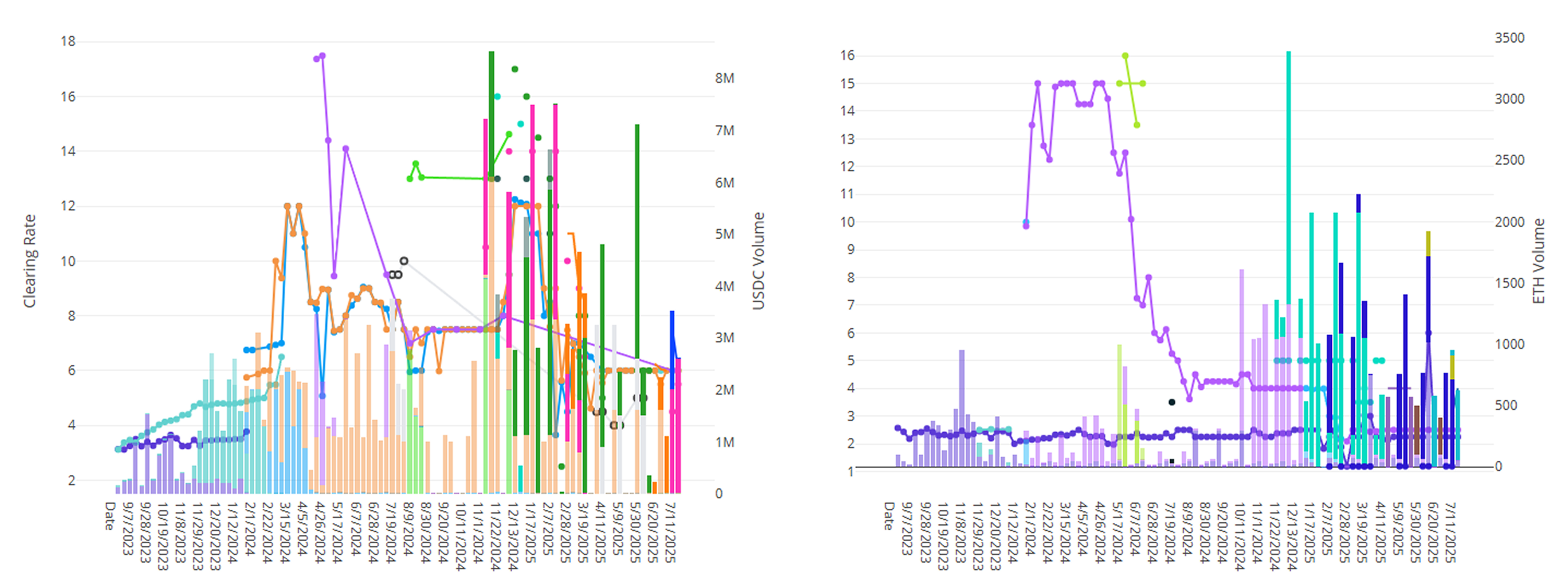

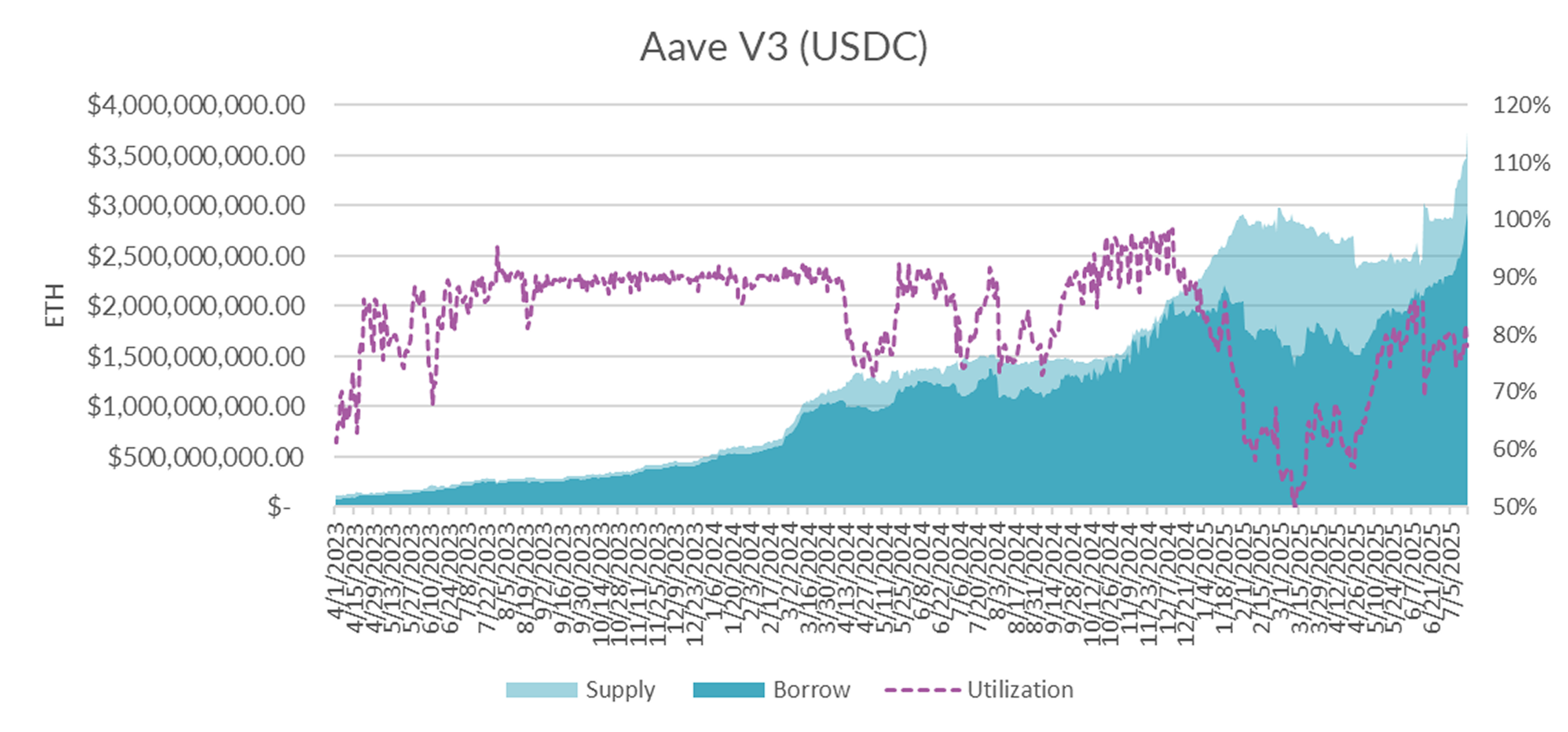

Diving into the microstructure of Aave's USDC markets, utilization held steady in the high-seventies, with both supply and borrow demand increasing around 500M, respectively.

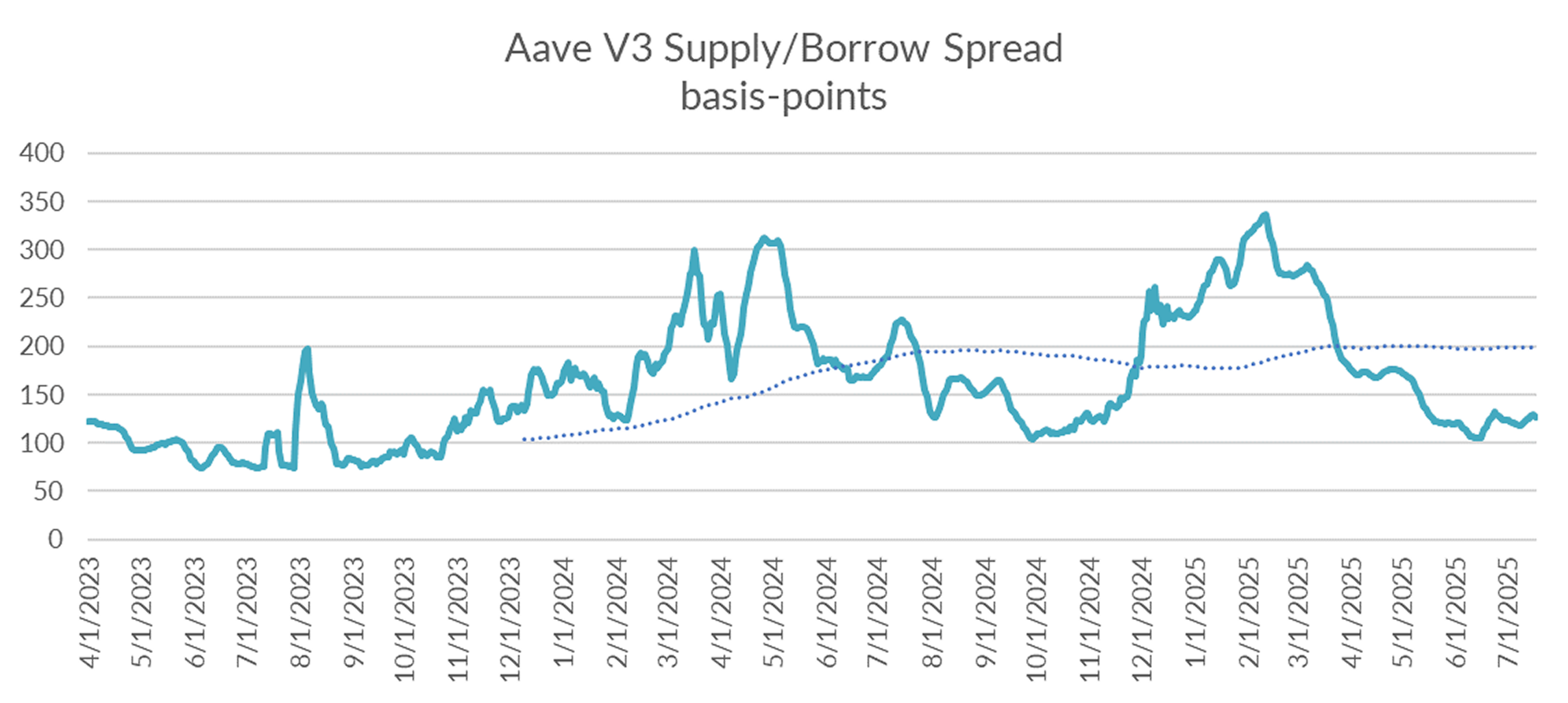

With the overall market relatively balanced, borrow-supply spreads remain near the low end of the range.

And while demand continues to increase toward new highs, total supply continues to maintain pace.

In the near term, markets appear relatively balanced but DeFi rates are expected to heat up as basis yields flow into DeFi.

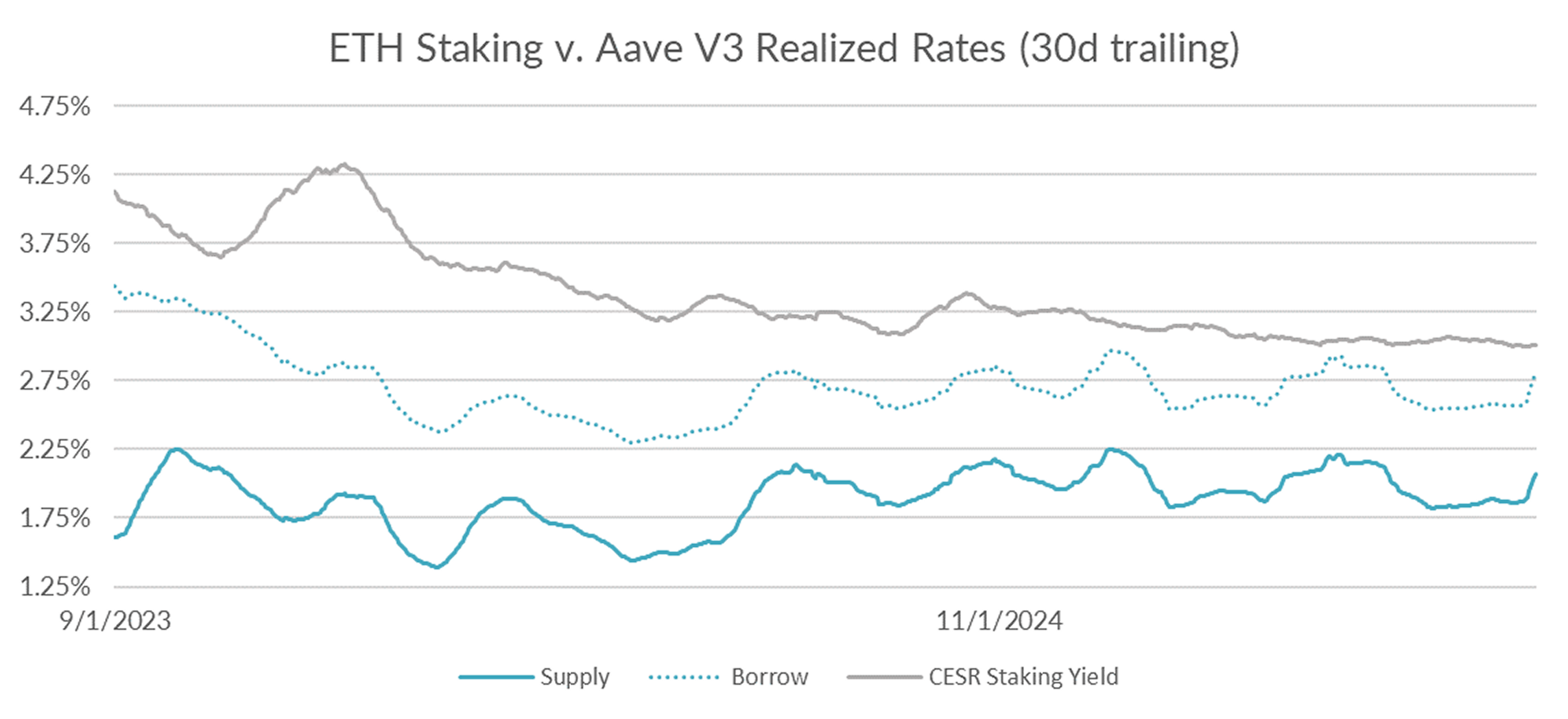

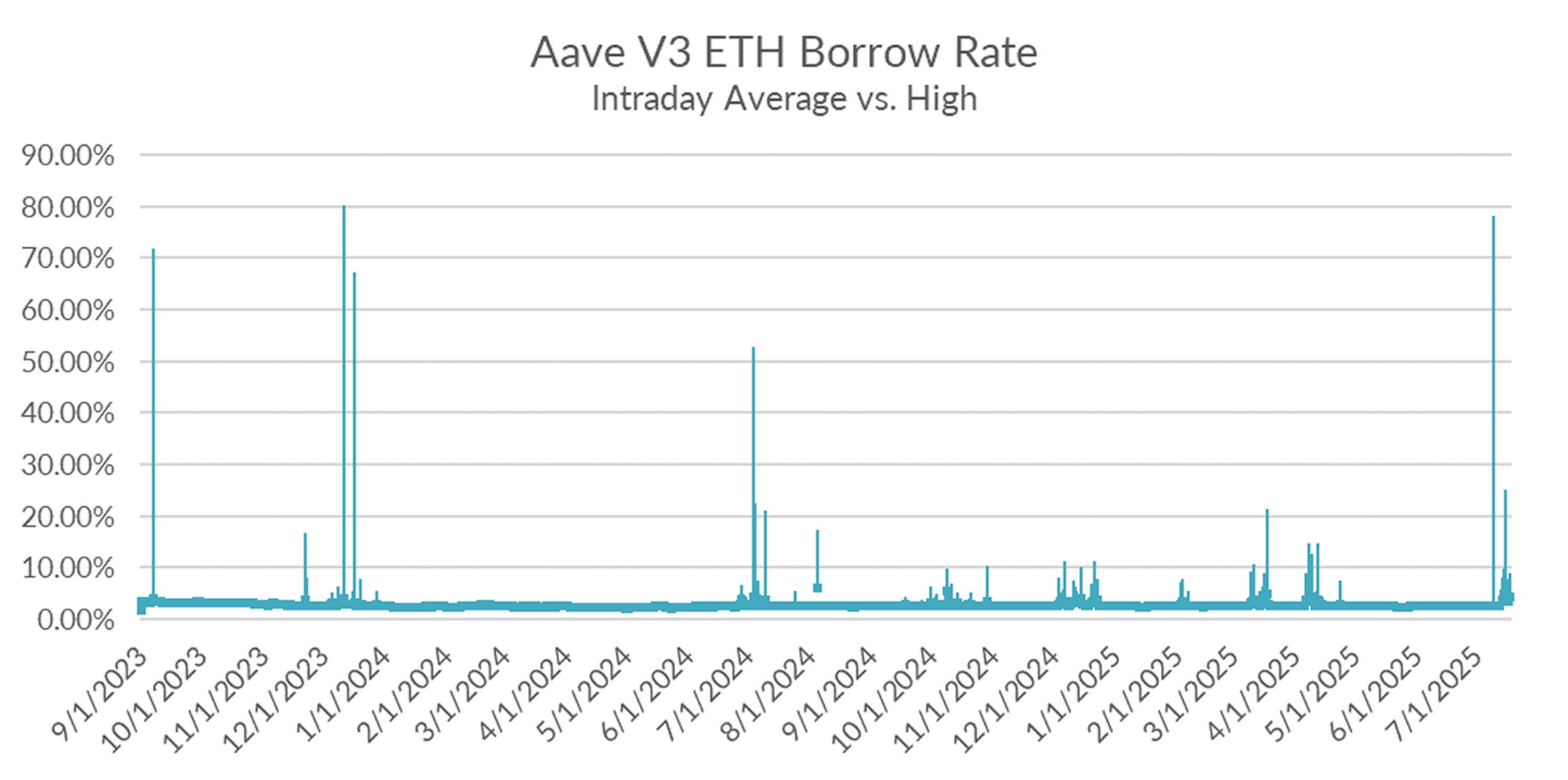

Turning now to ETH markets, ETH rates closed unch’ed on the week at 2.81%, up 24bps on a 30-day trailing basis. The CESR staking index, on the other hand, held steady at just 3.01% on a 30-day trailing basis.

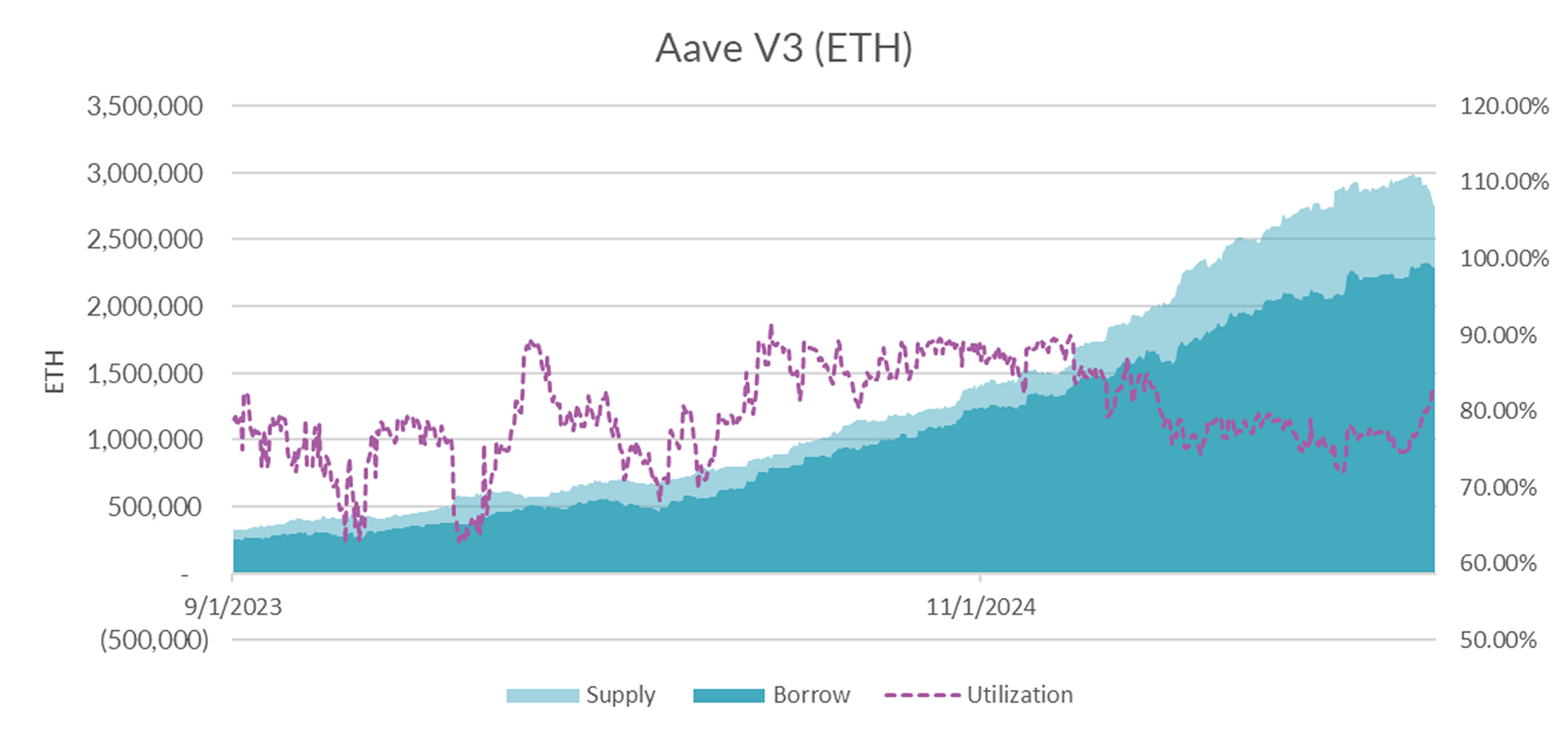

Market internals show that supply (-145k ETH) fell sharply for the second week in a row while demand also declined but at a significantly slower pace (-33k ETH) over the past week.

Diving into the intraday charts, we see that ETH borrow rates spiked as high as 19% APY intraweek and remains elevated as of the time of writing.

With ETH supply quickly declining, expect massive LST borrow loops to be unwound in the near future.

BTC followed through the breakout this past weekend and closes the week roughly unchanged at elevated levels. Alts, such as XRP and ETH rallied to make up lost ground against BTC in the current market cycle. Overall animal spirits and demand for leverage run high. Expect DeFi rates to pick in the near term.